Top performers see AI-powered growth

Often, it’s beneficial for founders to ignore the discourse, keep their heads down, and focus on building. With the bubble discourse, that appears to be true. Despite macroeconomic volatility and persistent questioning of whether the money is real, startups doing the work on the ground continued to grow last quarter, extending the broader uptrend we’ve seen across 2025. And, while the question remains whether venture is overspending, startups are keeping opex under control, and burn multiple is down for the second consecutive quarter.

We think that a lot of these gains are a result of AI. Based on the data from our Benchmark survey and prior flash reports, it seems that hyper-efficient GTM teams are leaning on AI to power their growth engines. Companies integrating AI into high value use cases are seeing meaningful movement in pipeline, quota achievement, and win rate.

At the end of the day, there’s no substitute for building a good business. The bubble will ultimately come down to pricing and valuations, not performance.

What you need to know:

- Growth is up Y/Y across the board, with the top decile continuing to operate at another level: While we saw improvements across quartiles, the top decile performers continue to pull away from the rest of the pack.

- Top growth = AI investment (we think). Opex over revenue is going down. Paired with our BenchmarkIt data that shows that 46% of teams using AI saw increased quota achievement and were 3x likelier to see an increased win rate, this paints the picture that increased growth is due, at least in part, to AI investment.

- Companies are investing in AI and remaining efficient. After two quarters of trending up, opex is trending down. We think this is representative of initial AI investment, which we’re now seeing the impact of in falling burn multiple.

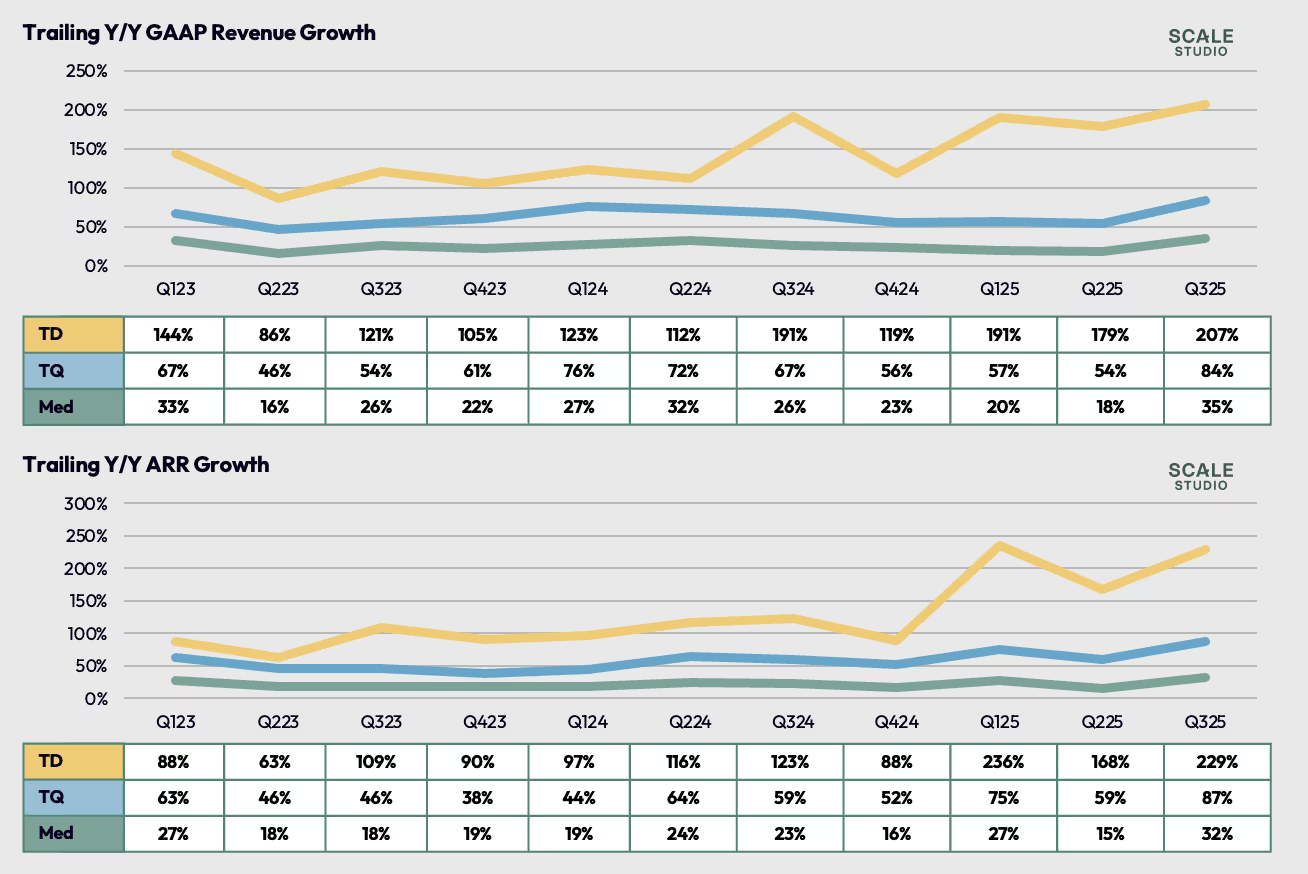

Both GAAP revenue and ARR increased Y/Y, but top performers continue to pull away

- Top decile Y/Y ARR rose by 61 percentage points, while the median increased by 7 percentage points

- GAAP revenue showed the same pattern, with every quartile showing higher Y/Y growth

- What it means: Startups across the board are growing, but the gap between top and median performers is widening.

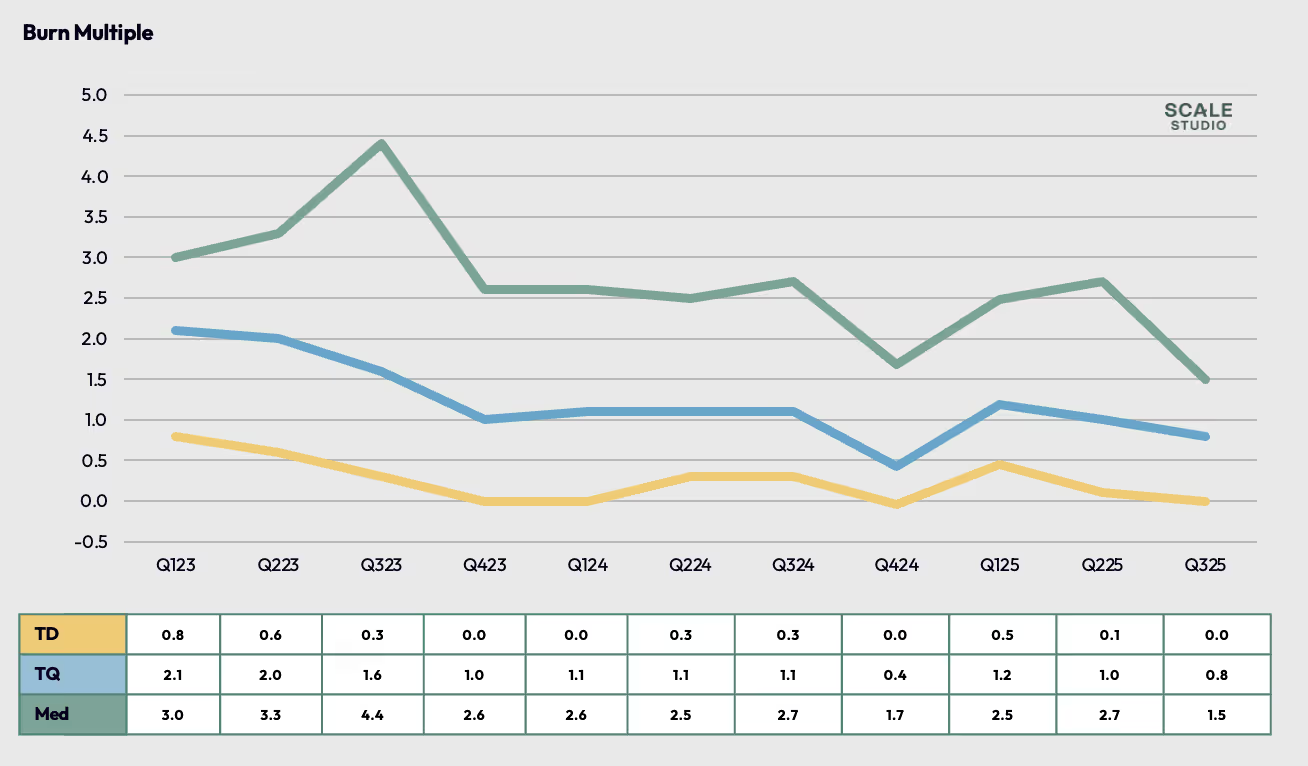

Growth does not come at the expense of efficiency as burn multiple continue to fall

- Top decile and top quartile performers saw burn multiple fall for the second consecutive quarter

- What it means: Startups are leaning into AI augmentation to boost efficiency and continue to do more with less.

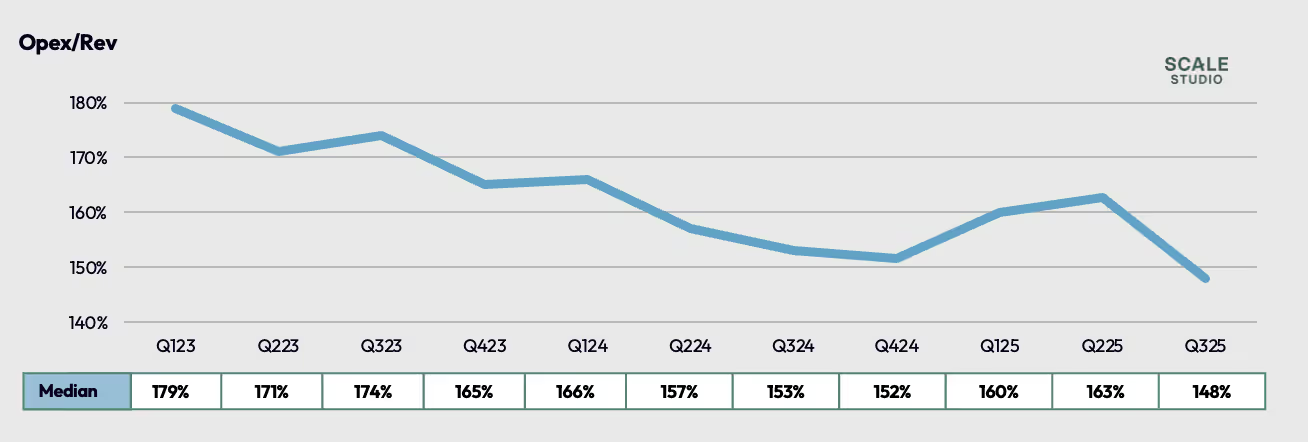

Opex/revenue declined this quarter, showing that operating expenses remain under control

- Opex/revenue trended down for the first time in two quarters

- We see that opex/rev declines over 2024 as an extension of the year of efficiency, but blipped in the first two quarters of 2025

- What it means: This trend could be attributed to rapid adoption of AI tools and hiring of GTM engineers. After a brief period of investment, efficiency gains are now starting to materialize.

News from the Scale portfolio and firm