Which AI verticals will have the next unicorn?

Vertical markets are having their day in the sun, thanks to enthusiasm driven by AI and the availability of LLM-based foundation models. I never would have imagined every venture fund having a vertical strategy even three years ago, but here we are. Having invested into these markets for over a decade, the truth is that “verticals” is a catch-all term and the distinctions between markets, say healthcare and trucking software, can be quite meaningful. My thesis is that we are only at the beginning of a significant secular trend, and that certain frameworks will help us understand the relative sequencing between these markets.

Let’s start with the obvious. Many investors have observed that LLMs are particularly strong at written language, that legal work is particularly focused on written language, and therefore concluded that legal markets are the first and most exciting for disruption. I agree and have been wildly impressed by new entrants like GC.AI, Harvey, Legora, and EvenUp. But knowing what went first doesn’t help in identifying the next five markets, or sub-segments that will see an explosion in AI. Said more bluntly, there’s little arbitrage (ever) in the obvious.

And if AI is not a two-year pop, but a significant restructuring of industries, we will want a framework that compounds over time. In 2008 Scale observed that cloud software would follow a risk curve: marketing software went first because they were creative and used to “testing,” sales thereafter, followed by HR software, and eventually finance software. Picking the leaders in each category at the right time (and not too early!) resulted in billions of capital gains.

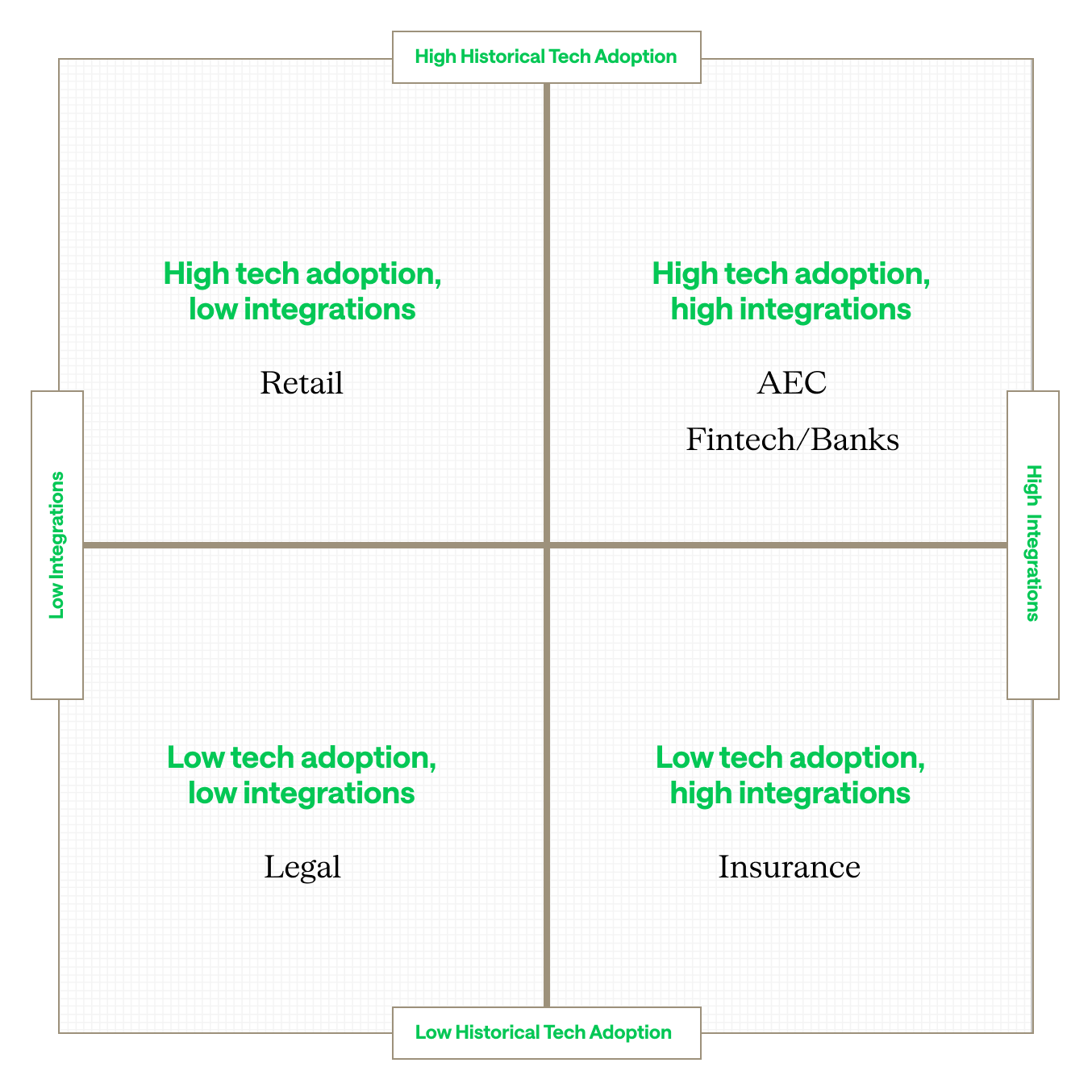

There are two main factors that drive speed of adoption: integration complexity and recency of tech disruption. The first wave of LLM-enabled (or native AI) companies in verticals mostly used a PLG motion, driving wildly rapid adoption at the individual or group level. As with any rule there are exceptions, but the key point is that value was ascertainable *without* integrations into existing systems. This allowed rapid decision making by buyers without corporate buy-in, or the necessary resourcing of customer engineering to deploy products. We love Freed as evidenced by our investment in them, and the brilliance of the product is that a doctor can purchase it with a credit card swipe.

Likewise, the early wave of native AI companies focused on industries that were laggards in the purchasing of technology over the past two decades. The last meaningful software many law firms purchased was the Microsoft Office suite, and likewise the explosion of notetakers in the healthcare industry is partially a reflection of the abysmal adoption of newer (and more user friendly) software by the healthcare industry.

These two insights combined create what I believe will be the AI adoption matrix that will unfold over the next decade. Verticals that require less integration and have seen less new software purchased in recent periods will be first to adopt, and verticals that require either deep integration, or were aggressive investors in early waves of AI, will be slower to adopt LLM-based innovations.

Note: The framework is not intended to be a comprehensive look at all relevant verticals but a snapshot of the framework in action.

Going back to our first example, no doubt the legal market has been successful because the heavy usage of written language is particularly well-suited for LLMs. But it’s also an industry where the step-function value and ROI of AI-based technologies has been incredibly significant. For example, most law firms still do not use collaborative document editors, whereas collaborative software is ubiquitous in much of the AEC industry. Likewise, most of the new wave of legal AI startups provide immediate value without integration.

Compared to legal tech, fintech has not seen any major native AI companies explode quite in the same way as other categories. Sure, fintech is an industry particularly heavy with numbers and tables, in which LLMs are not as strong, and compliance needs have presented their own set of challenges for adoption. But I believe the real reason we haven’t seen the early explosion is because the fintech ecosystem heavily invested in technology, including AI, over the past decade. Take JPMorgan, for example, who spends over $18B annually on technology, which exceeds the spend of all law firms in aggregate in the US. JPMorgan was an aggressive adopter of AI technologies such as neural networks and deep learning in the 2010s (including companies like Socure and Forter). There is no doubt that they are and will benefit from LLM-based architecture, but the gain in productivity is not as profound as in other markets, and therefore the ROI and change management will be slower and more complex.

Insurtech has a different challenge that has hindered the explosion of native AI companies. No doubt some segments such as brokertech will see the early winners emerge. But once you sell to carriers, you frequently discover that they have very complex data and software value-chains that influence the engagement with thousands, if not millions of customers. Companies like Sixfold have demonstrated that there are meaningful benefits gained from LLM-based solutions to assist in the underwriting process, and similar efficiencies can be gained in the incredibly expensive and cumbersome claims process. But that involves meaningful integrations into the existing systems these carriers have, as there is not a reality where an individual underwriter or insurance adjuster can bring on board meaningful technology. Their daily work is an ongoing stream of extracting data out of one system and inserting it in another system, and vice-versa.

Innovation is never linear, nor perfectly predictable. There will be break-out companies that contradict this framework, and there may be incremental factors that influence certain sectors to adopt even faster. No doubt, the influence of a strong incumbent should not be overlooked. If you’re in banking, the incumbent vendors of FIS and Fiserv are still struggling with their cloud solutions, whereas in hospitality, Toast is an incredibly dynamic, young company. This will both impact generative AI innovation, and whether that source is incumbent solutions or startup innovation.

All that said, I suspect that in five to ten years this framework will have been predictive of where we see successes. As alluded to earlier, it is not obvious to me that the first “winners” will be the biggest or best winners. Integrations are a form of moat, and so while high-velocity PLG-centric motions are incredibly attractive for growth, the complex burden of integrations are why many vertical systems have entrenchment today. The same will be true in AI. And while companies selling into sectors with some form of competition already will face more burden to deliver ROI, it will also force the early maturation of a GTM muscle that all great companies eventually achieve.

The net result will be a decade of entrepreneurial driven innovation that will redefine many vertical categories and is leaving the incumbency of these vendors up for grabs. It is a great time to be in verticals. Overall market euphoria aside, Scale has had an interest here for a decade, and will continue to invest over the next decade.

News from the Scale portfolio and firm