AI+Wealth management

As it turns out, asset management is a really good business. There are tens of trillions of dollars in assets being managed in the US across hedge funds, alternatives, mutual funds, and traditional financial advisors. With management fees generally ranging from a fraction of a percent to 2%, this means hundreds of billions of dollars in recurring revenue to be made—even more when you add in performance fees of the classic 2 and 20 model. Alternatives have gotten all the media attention over the past couple of years, but a real giant in the space is traditional individual financial advisory. There are over 300k financial advisors in the US with around $30Tr of AUM, and up until very recently they have been largely underserved by Silicon Valley. Maybe it’s because of the market size. If you multiply the classic $1k per head per year you don’t end up at a venture fundable number. Maybe it’s been simply overlooked by founders, due to the generally heavy single stock exposure of tech employees and rising stock prices that never made them think about advisory. Maybe it’s the classic verticals problem of deeply entrenched incumbents with a suite of products and services that has been too daunting to compete with.

Much like other white collar categories, wealth management is seeing immense AI-driven innovation that is exponentially increasing the TAM, blowing up incumbent moats, and driving bespoke, human-powered services downmarket through innovation. But before getting into how AI can help advisors better serve their clients or talking about tech-enabled services, it helps to understand financial advisory as a whole and just how much tech they interact with today.

A history of financial advisory: from wirehouses to the independent RIA

All the way back in the late 1800s / early 1900s, if you wanted to buy stocks on an exchange, you needed to go through a broker. And if you lived far away from the exchanges, the only way the brokerages could relay your purchase order back was through telegraph or phone, which is how the wirehouses got their name. You picked what stock you wanted to buy, or your broker would call you up with a very promising opportunity, and you would place an order with your broker, who would collect a fee for their service. This premise remained largely the same all the way until the end of the 1900s, with a bit more fragmentation in the market toward the end of the century as the internet and electronic exchanges became more widespread. Incentives were largely not aligned. Your broker didn’t really have to care if the stock went up or down; they collected a fee every time an order was placed. The wirehouses remained the dominant players in this market through this time, as their size allowed them to offer a lot of various financial products, and their armies of brokers could sling cold calls all day trying to sell structured products or shares in the latest hot company. The original wirehouses all still exist in some form today: Merrill Lynch became Bank of America’s brokerage and investment bank, Paine Webber is now part of UBS, E.F. Hutton’s and Bache’s lineage largely traces to Wells Fargo. Morgan Stanley’s wealth management history started a bit later, largely built by their own and Smith Barney’s efforts in the mid to late 1900s.

Like many innovations, the wealth management category evolved out of misaligned incentives. Many brokers wanted the best for their clients, to give them proactive financial advice, and for their compensation and boss’s praise was tied to how well their clients performed. Clients wanted that too. How do you really know if your broker has your best pinterest in mind if they get paid whether you make or lose money?

Enter the independent financial advisor. These existed before this period, but the late 1990s and early 2000s were the beginning of a large change in the industry, where brokers and advisors shifted away from wirehouses to independent shops and smaller financial institutions. The premise of an advisor (as opposed to a broker) was that they would collect a fee on the total assets managed for a client, so incentives were aligned. Now if the advisor picks good stocks and the client’s portfolio grows, they both make money.

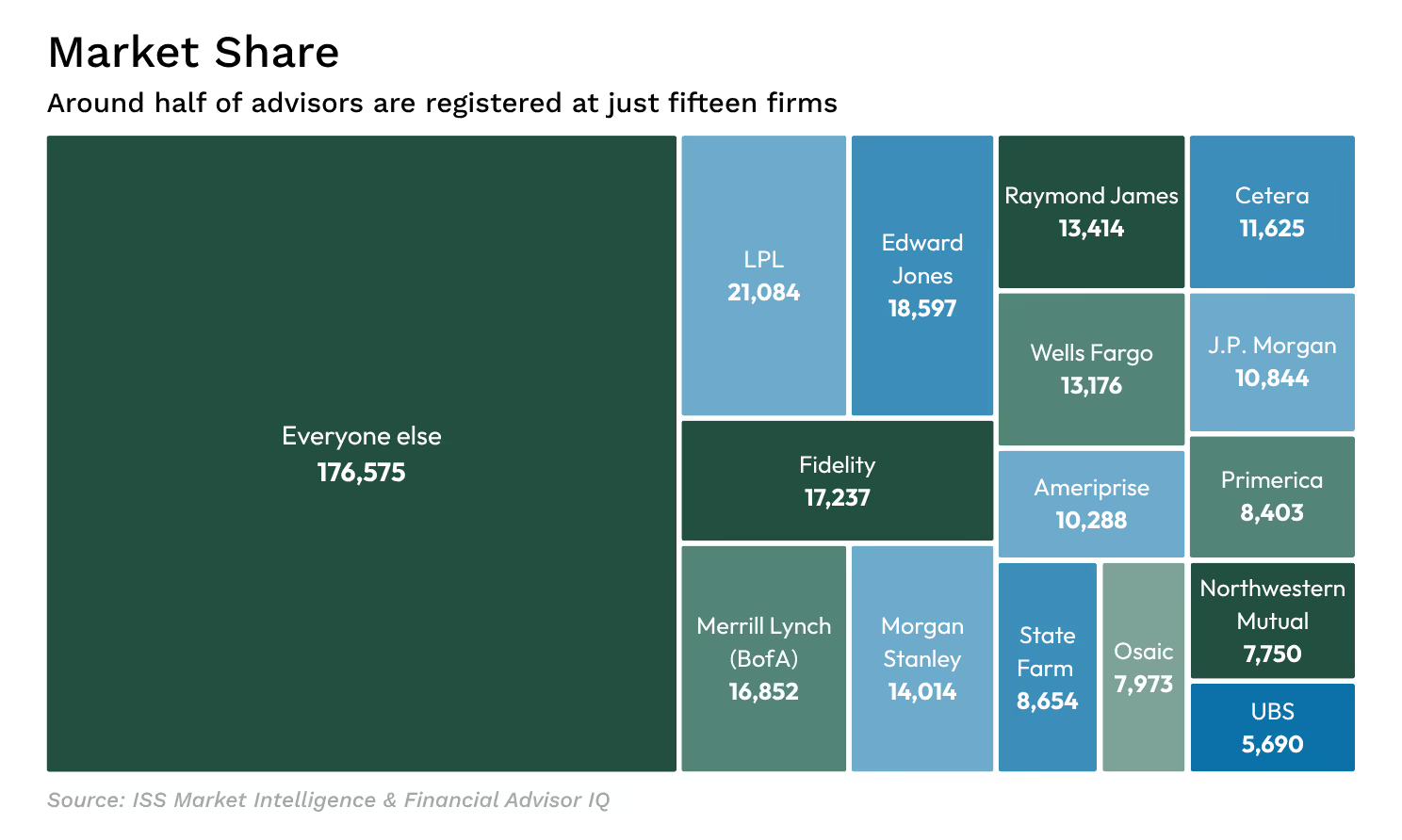

Many independent advisors operate as part of a larger platform such as LPL, who can provide the tech stack and back office support advisors need to run their business so they can focus on their clients. Today, most advisors work outside of traditional wirehouses, and independent platforms continue to grow market share.

The financial advisor tech stack

A typical financial advisor interacts with four core, market-specific pieces of software or services: a CRM, financial planning, portfolio management, and a custodian.

CRM: Ultimately, financial advisory is a sales job. You need to convince people that you are worth roughly 1% of their portfolio every year to be successful in the space. So the CRM is one of the most important tools they use. They use CRMs like Salesforce Financial Services Cloud along with some more advisor specific products like Redtail (Orion) or Wealthbox.

Financial planning: Financial planning is where advisors help their clients with strategic longterm planning, largely focused around retirement. You can project the balance of your portfolio, estimate how much you will be able to spend every year in retirement, and pressure test with surprise medical bills or lower returns to see how that flows through. The large players in this space are eMoney (Fidelity) and MoneyGuide (Envestnet).

Portfolio management: If financial planning is strategic, portfolio management is a much more tactical way for an advisor to look at a portfolio. It shows all your client’s holdings, performance on each, and risk scoring, and it can generate the reporting needed to send to clients. They can also help with billing, as it tracks the value of the investments and transactions made for both management fees and commissions. The largest portfolio management products come from Envestnet, Orion, and SS&C.

Custodian: The custodian is where the assets are actually held. Custodial services are generally provided by the largest broker dealers and used by every other advisor, as the SEC dictates that assets must be held by a custodian. Every change to a client’s portfolio of public securities will move through the custodian, so it can’t be overstated how important reliability and security are here. It doesn’t make sense for sub-scale companies to be custodians given stringent regulatory requirements, so it is reserved for firms like Charles Schwab, Fidelity, LPL, and a relatively new entrant to the space, Altruist. The custodian is also the only piece of the core that can monetize AUM instead of just seats, indirectly by monetizing uninvested cash through cash sweep and directly by charging a fee on proprietary products.

This is just the beginning. Once you get into specialty planning like tax, estate, or education, you will need to interact with a specific piece of software for each. You need more horizontal financial services tools like investment data and compliance. And there are all the broadly horizontal solutions most businesses need, like e-signature, document management, billing, and sales and marketing tools. All in, an advisor could end up interacting with 10+ different products on a regular basis.

With all the tools needed by a financial advisor, some very large incumbents exist in the space. The largest, which have products in almost every piece of tech an advisor could want, are Envestnet (recently taken private for $4.5Bn), Orion, and SS&C Black Diamond. Unsurprisingly, all of them are PE owned and all of them were founded before 2000. Each of them started owning one of the core four areas and have expanded their offerings from there. These are very entrenched companies in financial advisory with such a wide range of products that it becomes really difficult to replace them. That doesn’t mean that selling software to advisors leads to a dead end—by and large, the incumbents are not innovating—but startups have needed to get creative about creating value outside of these product suites, which could leave the incumbents exposed. You could also think about starting from the ground up and creating an advisory firm with an in-house modern tech stack to improve on legacy products.

What’s happening now: innovative asset management and the AI enabled advisor

Point solutions alone don’t work in this market because the size is not large enough. So the approaches are 1) get part of the transaction stream as some form of advisor, 2) sell across the tech stack and into one of the four big buckets of software using a high ROI first product to get your foot in the door, or 3) automate the work so you can start replacing time spent on back office and admin tasks.

Tech-enabled advisory

So what can a firm look like if you decide to start from scratch? It can take a number of different forms, all with the same pre-existing goal of giving peace of mind and risk adjusted returns to their end clients. There’s Savvy, Farther, and Compound who look most like a traditional independent financial advisor, but with a belief that if you can build your own in-house tech stack you can get meaningful gains in the two drivers of success for an advisory firm: number of advisors and AUM per advisor. In addition to a modern tech stack being a better experience, this also allows these new age advisors to more easily layer on AI products in client engagement and sales and marketing to reduce a lot of the admin work that goes along with prospecting new clients and growing their book. Compound is taking a slightly different approach to this, but mostly in who they target as end clients and with more of the value added services that come from the family office approach to advisory.

Then there is Range, who is taking a fundamentally different approach to the financial advisory space by getting rid of the advisor-client relationship and leaning on a self service model, with AI doing much of the work an advisor has historically done. And because it’s much less headcount intensive and less hands on for the client, they charge flat annual fees instead of charging based on AUM. Today, I think about it as human-in-the-loop robo advising: when the user encounters an edge case, an advisor steps in when needed for more complicated services. We expect this segment of advisory to evolve, with full-service agents taking over more of the work and changing the economics in this space (Range is already running a promising beta).

Automated advising

General roboadvising has been solved by companies like Wealthfront and Betterment by providing a nice and easy way to build your own 60/40 (or 80/20, 50/50, etc) portfolio of equities and fixed income products so you can end up in largely the same portfolio an advisor would put you in but for ⅓ to ¼ of the fees. The opportunity in the automated investing space requires taking a novel approach beyond standard portfolios and vanilla products. One clear avenue is to take the financial products that are very expensive and only available to high net worth clientele and bring them down market with the aid of technology. A company taking this approach is Cache, who is solving the growing problem of single stock exposure for long-time tech employees and helping them diversify without having to sell their shares and trigger capital gains tax. They are doing this through an exchange fund, in which people with very heavy exposure to specific stocks all come together and put those shares in a pooled vehicle that they get an ownership stake in, diversifying their portfolios without needing to sell anything. Because this is a much higher value service than buying off the shelf ETFs for you, they can charge 0.5% – 0.95%, much more than the 0.25% Wealthfront charges but still a lot less than the 1-2% that this would traditionally cost. Another approach is to bring active management downmarket by outsourcing the stockpicking to those you trust with much simpler pricing models and availability to the masses. Autopilot and Dub let you invest alongside some of the best individual traders like Nancy Pelosi through platform or user constructed portfolios. For a flat subscription fee of less than $100 a year, you get access to a number of actively managed funds giving retail investors a hedge fund like product without the high fees and redemption restrictions.

Efficiencies in high-value workstreams

For selling software to advisors, you can generally think of it as helping the advisor serve their client or helping the advisor get more clients. Specialized planning tools fall on the side of helping advisors provide more and better services for their clients by giving them either net new capabilities or a much more streamlined way to handle more complex tasks in advisory. Estate planning, for example, is traditionally a very time and document intensive process, which makes it a perfect candidate for an AI solution to drastically cut down the amount of work required by the advisor. Vanilla, Wealth.com, and Luminary are all focused on making estate planning a much simpler process for advisors, which helps advisors who already handle estate planning serve more clients and enables new advisors to offer estate planning. These products save so much time for advisors that you can generally charge premium prices compared to more common tools in the advisory tech stack. They greatly expand the number of advisors that can now offer this type of planning and if the experience is simple enough, the DTC door can open as well, which starts to make the market size attractive. We think the most exciting next steps for these companies are to start tackling more types of specialized planning like tax or education or to offer their product outside of financial advisory to other parties in the estate planning process like accounting or legal companies.

GTM pipeline

Financial advisory, at its core, is a sales job: the more clients you can reach out to and the better you can prepare for your meetings, the more you can organically grow your AUM and collect more fees. But prospecting is hard. Most of the people you reach out to don’t want to talk to you, so finding some way to automate the outbound and find higher intent leads can allow advisors to find more potential clients and spend less time doing so. Companies like Cashmere and WealthFeed are trying to solve the prospecting problem for advisors, helping them build their pipeline through better identification of leads, prioritizing them, and aiding in outreach. Traditional lead gen already exists in advisory, but AI prospecting tools can offer this service for cheaper and at higher volume, and start giving meetings to the advisor as they can automate outreach to potential clients. Once an advisor gets a meeting with the client, they need to prepare for that meeting and spend admin time afterward logging it to the CRM and noting any follow ups. And if you have more client meetings from an AI prospecting tool, you have more admin work. Jump, Zocks, Focal, and Warmer all help advisors with the pre, during, and post client meeting work helping them prepare, take notes during the call, upload to the CRM, and plan next steps. As these products automate more of the sales work of an advisor, the advisor needs to interact with the CRM less and less, which can leave room for these new systems of engagement to become the system of record and start to replace the products they integrate with today. By capturing client interactions and changes they wish to make, there is also opportunity down the line to push these changes directly into the financial planning or portfolio management systems, eating more of the core system workflows.

Closing thoughts

As it turns out, asset management is a really good business, and one that is often overlooked from a technology perspective. Fintech is a hard market to break into, and as a SaaS market, financial advisory wasn’t big enough to be appealing. AI is changing that, opening up TAM through enabling expanded offerings and allowing services to move downmarket, as well as make productivity gains. There’s also some interesting space in building a tech-first advisory from the ground up. We are similarly excited by those trying to collect AUM like a multi stage venture capital firm or those selling products to advisors that enable them to better serve their clients and serve more of them. If you’re a founder or investor in the space or a financial advisor that likes trying new products, I’d love to chat. You can find me at damian@scalevp.com.

News from the Scale portfolio and firm