Out of the hype cycle: Fintech's reversion to the mean

At first glance, things in fintech don’t look great. Since the highs of 2021, we’ve seen few successful public market entrants, a pullback in valuations, fintech giants sitting under water, and a precipitous decline in venture funding. So, are things really as bad as they seem?

We pressure tested the “fintech is dead” narrative by taking a look at category-level funding to see what recent funding trends say about investors’ interest in the vertical. We found that while specific sectors have seen a sharp funding depression over the last few years (crypto, neobanks, and lending), dollars flowing into other categories such as payments, asset management, insurtech, and B2B fintech SaaS have stabilized back to 2019 levels. So, while some of the more volatile categories have not recovered, interest in core B2B fintech measured by dollars invested remains stable.

Fintech as a whole

The contraction in VC funding in the last two years did not happen in a vacuum. As interest rates began to rise in early 2022, public multiples contracted, which signaled an end to easy money and the “growth at any cost” mentality across the board, but especially for fintech companies. Private markets lag publics in valuation resets, but one of the best indicators of how venture investors view the continued attractiveness of the fintech sector can be seen by looking at category-level funding levels over the last few quarters.

Examining the data more closely highlights just how extreme the funding glut was over the last few years (below Pitchbook data shows total fintech fundings in the US, Canada, and Europe over the last 5 years).

Tracking this against the F-prime Fintech Index (an excellent resource that shows the combined performance of ~50 publicly traded financial technology companies), you can see the private and public markets operate almost in lockstep. Steady funding, rash exuberance in 2020-2021, and a commensurately swift decline starting early 2022.

Down, down, down

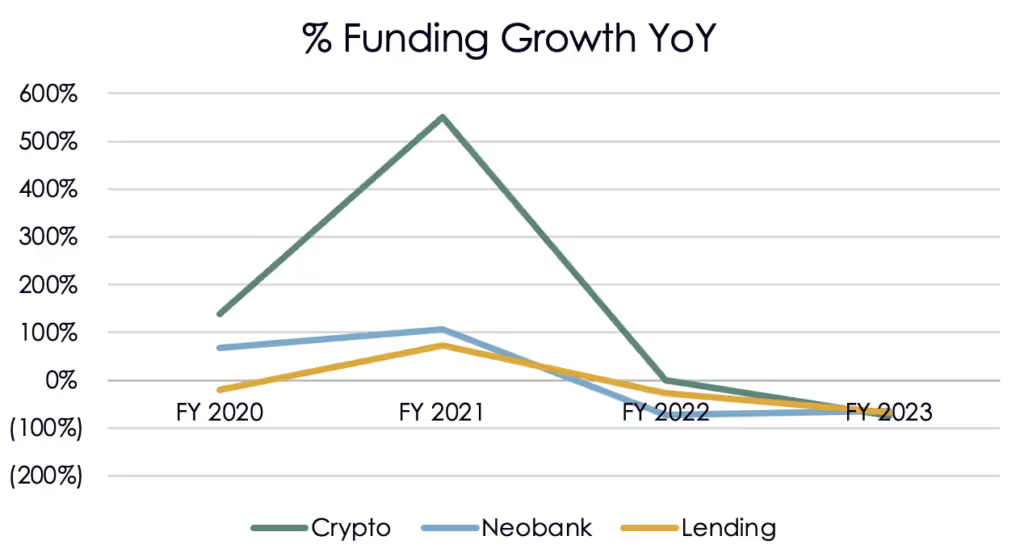

Part of the reason the fintech slump has seemed so extreme is the rapid rise and fall of a few specific subsectors. Crypto, neobanks, and lending were three of the hardest hit sectors over the last couple years.

Funding to fintechs in crypto rose rapidly YoY in 2020 and 2021 (grew >550% in 2021 alone) and subsequently flatlined in 2022, with a decrease in dollars flowing into the sector in 2023 (down 73% compared to 2022).

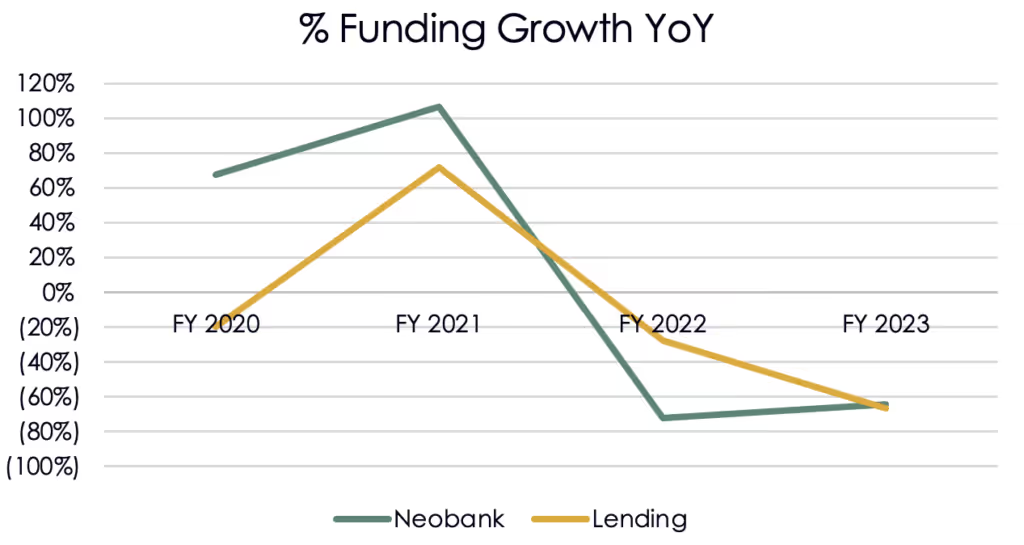

Neobanks and Lending categories have seen a similar pullback, albeit not as dramatic from a percentage growth perspective. Venture dollars flowing into neobanks have dropped ~70% each of the last two years, while dollars flowing into lending have seen an accelerated decline in nominal funding through 2023.

From a purely dollars funded standpoint, what does this mean? In 2022, Crypto, Lending, and Neobank financing rounds represented ~50% of total fintech dollars deployed and ~$20B of invested capital. This has now been halved to less than 25% of total dollars invested in the space, with ~$6B invested in 2023.*

A reversion to the mean

The good news is, things in core B2B fintech have normalized. Omitting the more dramatic declines in crypto, neobank, and lending verticals, we’re left with what we have termed “broader fintech” i.e., fintech fundings that do not fall into the above categories. Breaking what’s left down further into sub-categories of Payments, Asset and Wealth Management, B2B SaaS Fintech, and Insurtech (what we broadly consider to be core B2B fintech) reveals some interesting trends.

Funding in these sub-categories has experienced less volatility than those in crypto, neobanking, and lending sectors. While 2021 still represents an all-time high in dollars invested, 2023 actually saw year-over-year net increases in dollars deployed into payments and insurtech, with aggregate dollars invested in the categories here staying about stable over the last two years (~$20-22B).†

If you compare overall funding in core B2B fintech over the last five years, you can see that while these sectors were not immune to the avalanche of funding in 2021 (and subsequent drop back to the mean), things have stabilized with a reversion more akin to 2019 funding levels over the last 18 months.

2024’s fintech future

Fintech was not immune to macroeconomic forces over the last four years, for better and for worse. In some cases, cheap capital fueled by a zero interest-rate environment encouraged companies to chase growth with little regard to unit economics and profitability. These companies have had to march back excess spending and find their footing. Valuations soared in both public and private markets as optimism was buoyed by large exits in the space, and these valuations have come down from their 2021 highs.

Still, we believe that the best investment opportunities in venture are as elusive as they are resilient, and that financial technology is no exception. While rising interest rates, multiple compression, and a flight to profitability have in some cases dampened investor interest in sectors that are more directly exposed to these changes, the fintech category is still full of opportunity.

Over the last decade, we’ve been consistent investors in broader financial technology having led rounds in Bill.com (accounts payable), Socure (KYC), Forter (payments fraud), and Papaya Global (global payroll). In 2024, we are particularly focused on the areas of money movement that have remained expensive, prone to fraud, and are relatively untouched by horizontal fintech solutions that have proliferated over the last few years. These include software-led vertical payment networks, applications of cross-border money movement, and, of course, applications of automation and AI serving the category. In the decade to come, we look forward to supporting entrepreneurs in the space as fintech continues to grow — albeit, a bit more sustainably this time.

News from the Scale portfolio and firm