Liquidation Template 3 - Participation Uncapped

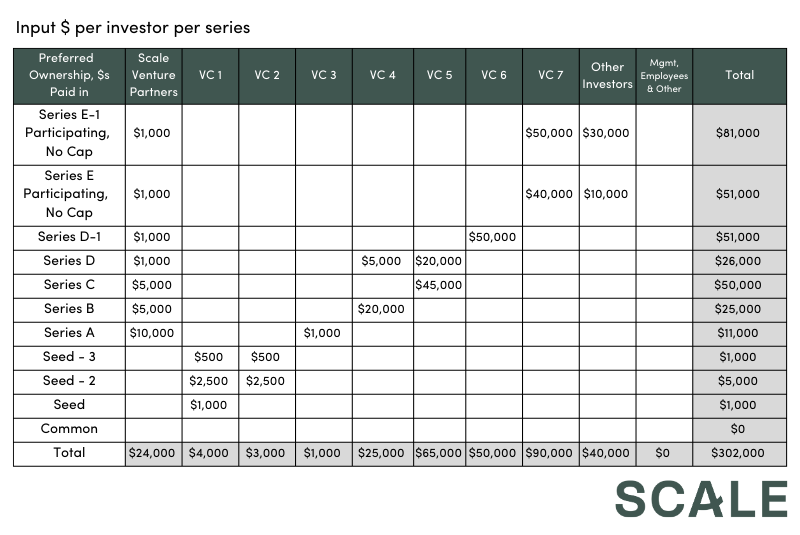

This is the accompanying template to our Liquidation Survival Guide Vol. 3. The goal of this guide is to help entrepreneurs, venture capitalists, and any others who are entangled in the nitty gritty details of modeling these complex liquidity situations.We talked about the base case with non-participating liquidation preference in volume 1 of this guide, and in volume 2 we added seniority to our cap table to understand its effect. Now, it’s time to get into the more onerous preference of participation. When we walked through the proceeds distribution before, the logic for each series was to determine if investors would receive more returns by keeping their preference or by converting to common shares. At the core of it, they had to make a choice.With participation, they don’t have to make that choice and can get their preference while also participating in any common. Essentially, these series are double-dipping! This significantly juices the preferred returns of these participating series and reduces the non-participating preferred series and common returns.There is also a mechanism called a participation cap to attempt to limit the consequences of participation on the rest of the shareholders. Think of no cap as unlimited double-dipping versus a cap as double-dipping to a certain point. When a cap is introduced, the analysis becomes much more complicated, so let’s first start with no cap in this guide, then in volume 4 we’ll walk through participation with a cap.This guide is to empower founders, VCs, and others in the ecosystem to better understand how structure proposed by investors will affect the cap table and distributions. The key questions we’ll answer are:

- How do we account for these two participating preferred series receiving their preference and common, no matter what?

- How does this double-dipping impact the rest of the shareholders?

News from the Scale portfolio and firm