Q1 flash update: Startups are back on offense

It feels rough out there, at least from the headlines. But despite broader market volatility (liberation day anyone?), early indicators from software startups show signs of resilience. Startups are going for it, and willing to take some hits on efficiency for gains in revenue.

What happened this quarter:

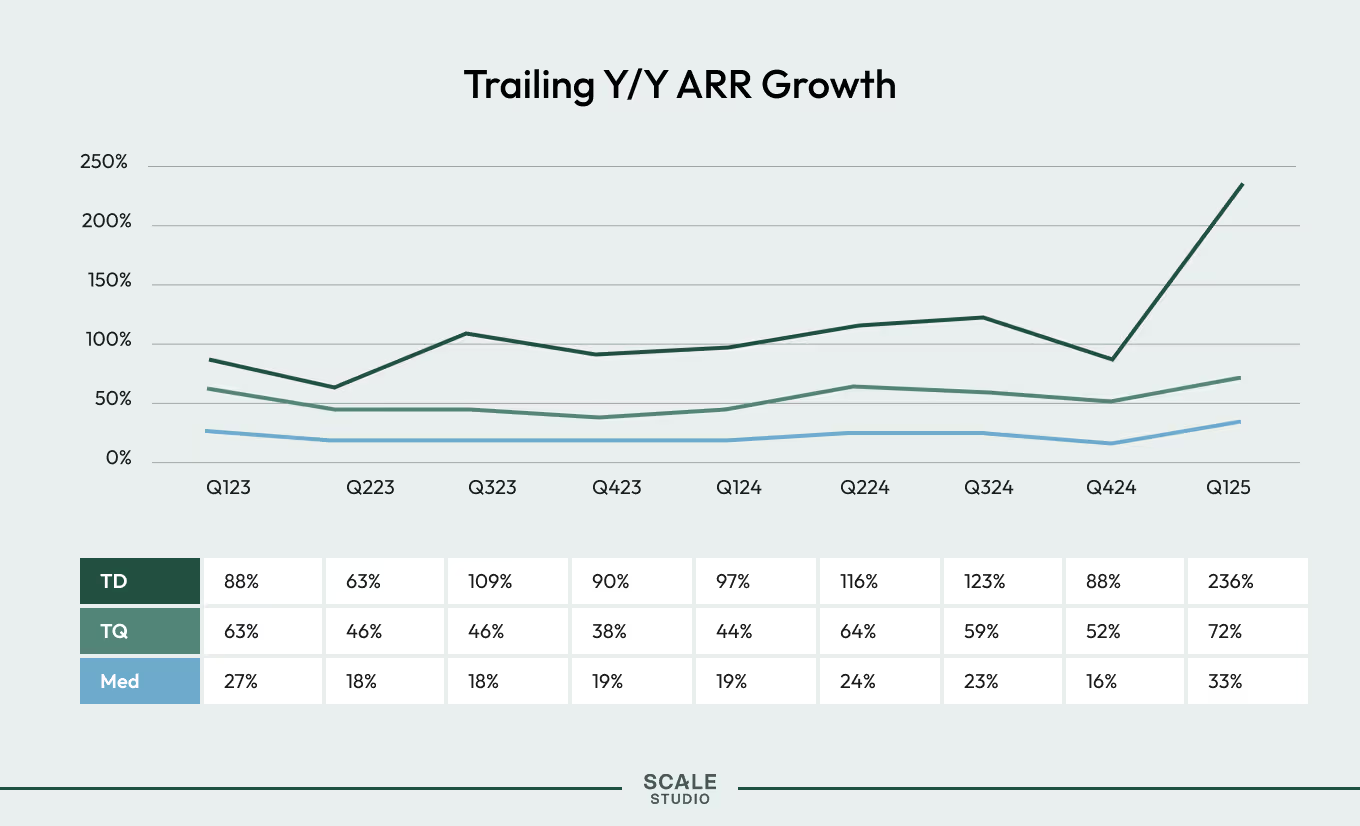

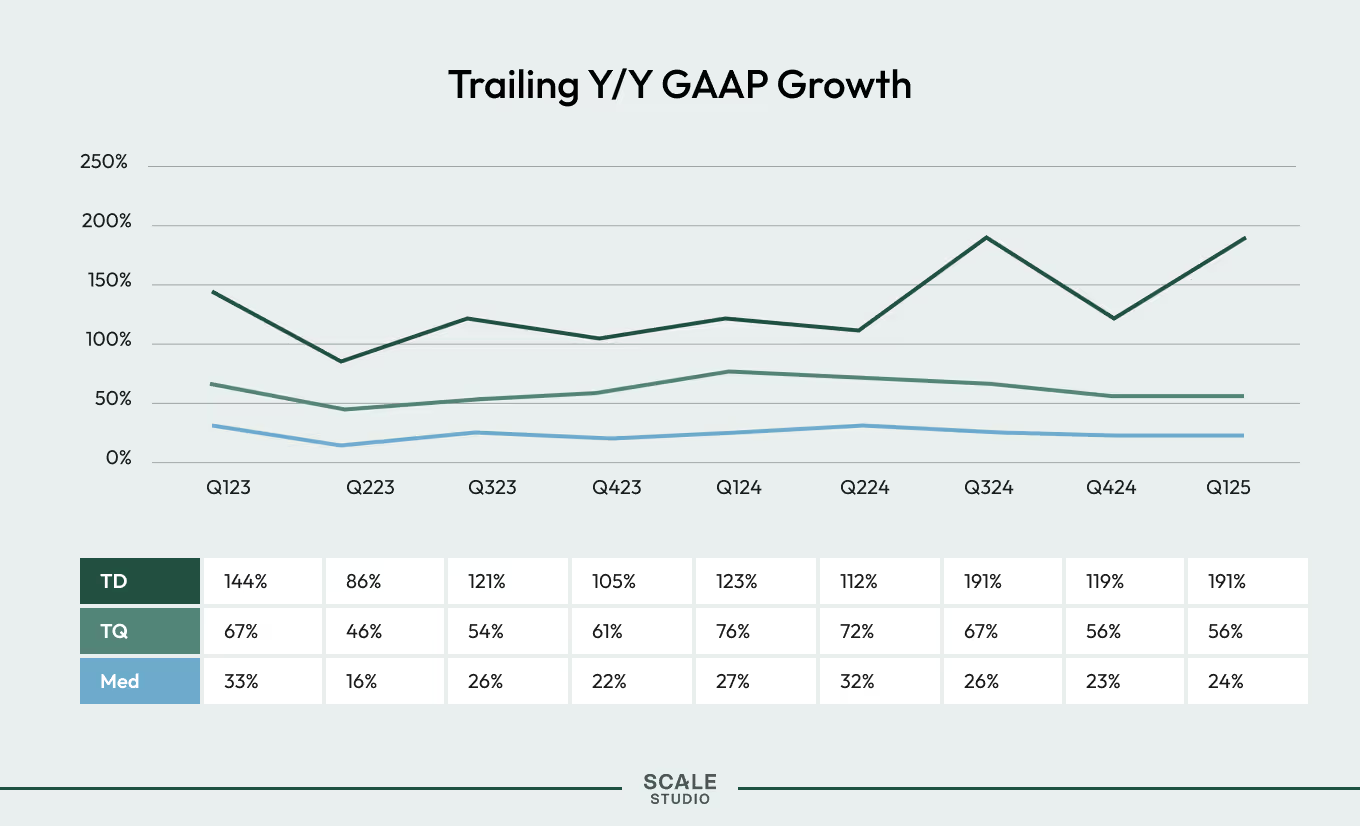

- Companies are back on offense. Both ARR and GAAP growth accelerated this quarter, with the top decile pulling meaningfully ahead.

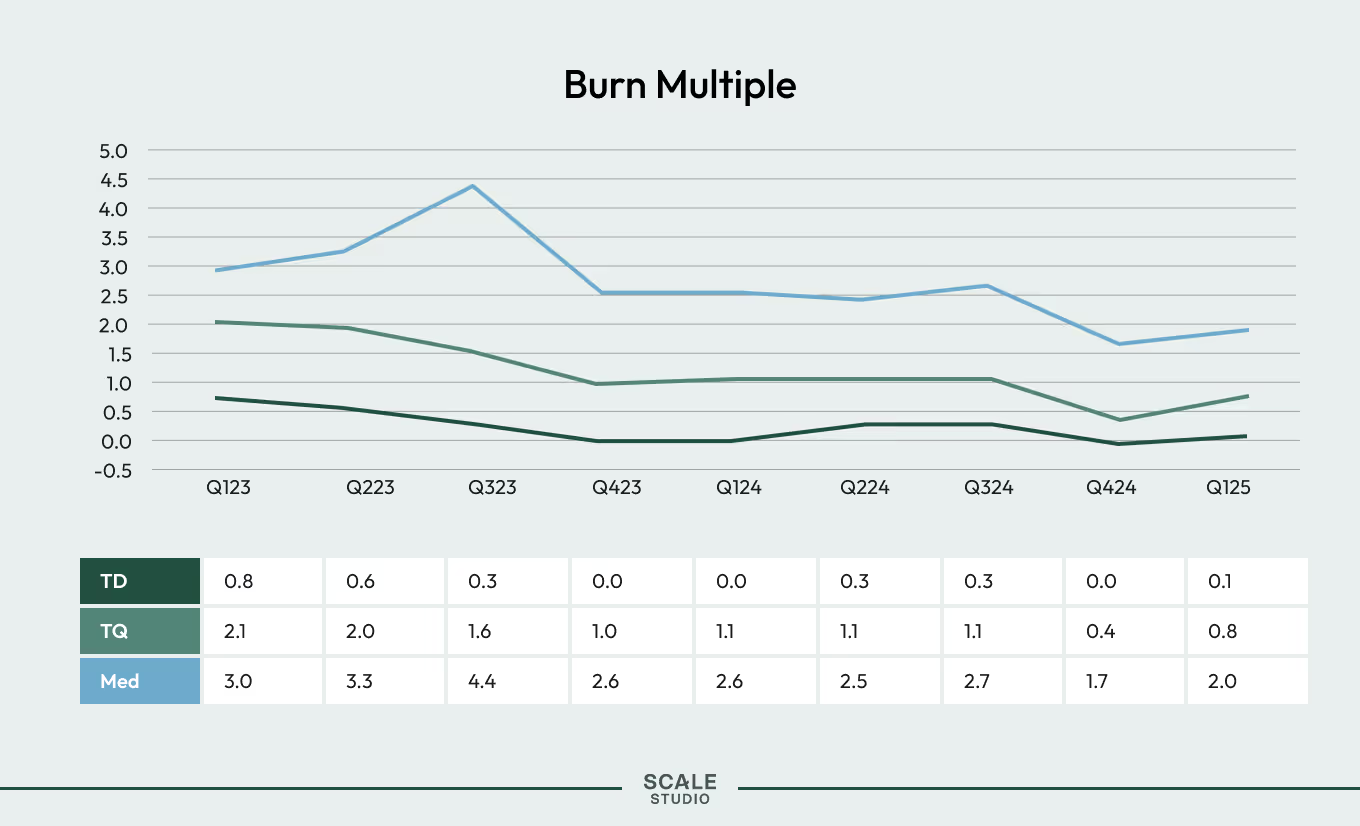

- They’re taking on more risk for a chance at more revenue. Efficiency decreases, while spending picks up slightly. After two years of belt tightening, burn multiple crept up. Either we have gotten all the juice we could squeeze or startups are getting comfortable taking risks again (or both).

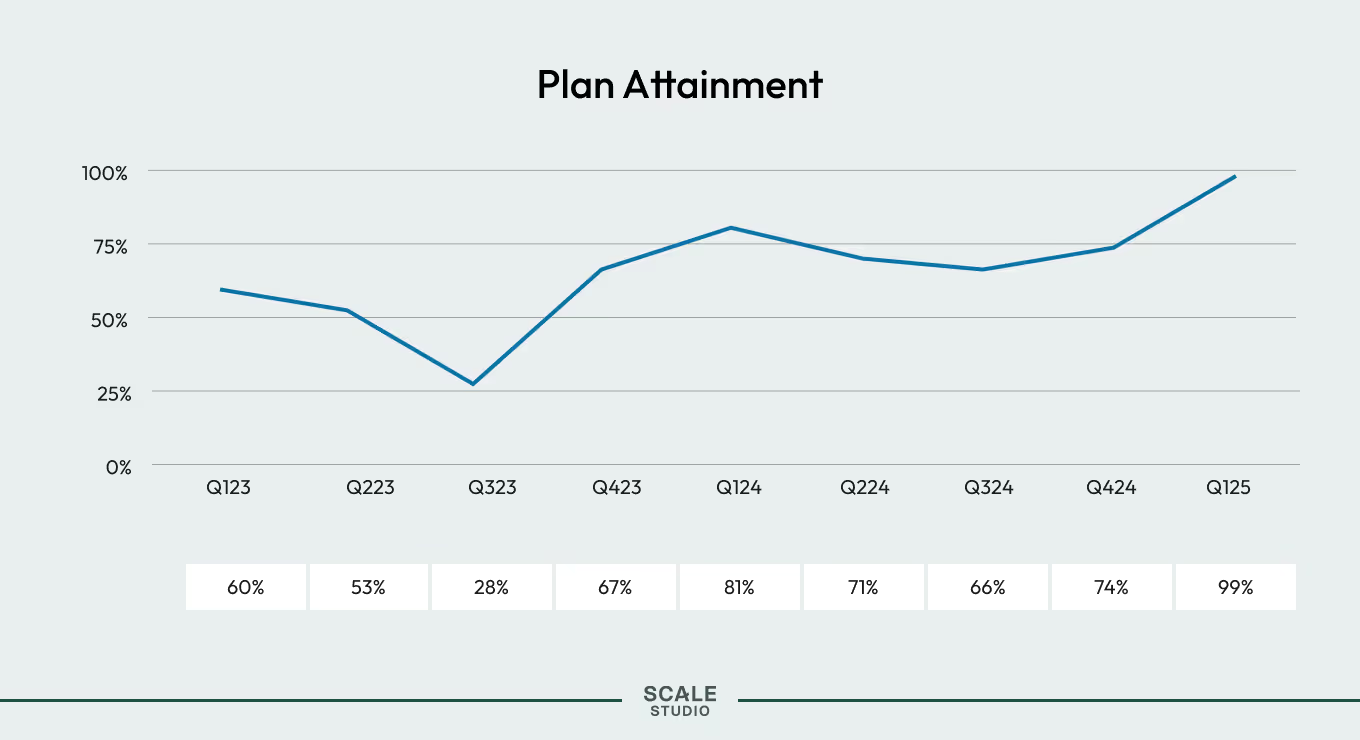

- (Almost) everyone is operating on schedule. Plan attainment was 99% this quarter, up from 74% last quarter. Founders (and boards) are setting the right expectations for the moment, and execution has been solid in getting them there.

Startups, for now, seem insulated from the whiplash of the public markets. Growth rates year to date are improving. Efficiency gains are starting to level off, but companies are clearly shifting back to offense. They’re spending more, sacrificing a bit of efficiency, and leaning into growth—just not like the drunken sailor era of 2021.

2025 will test if renewed spending will convert to real ARR. Big picture, it’s possible that we’re in a period where the only guaranteed failure mode is not pushing toward growth. The fallow period of 2023—when nearly everyone pulled back on spend, growth, and hiring—looks like it’s behind us. In the private sector, more startups are tracking to their annual plans, taking the first step towards another year of accelerating growth. Right now, it’s not about seeking shelter from the storm but playing to win—while making sure you have enough runway to keep your seat at the table.

It’s worth noting that tariffs are a wildcard currently not represented in the data. We expect to see their impact start to emerge in the April data. We’ll share early data when we have it in a few weeks, and in full in next quarter’s flash report. But, consider this a gentle warning that if you rely on chips or any other physical asset to run your company, it’s probably time to go on defense.

2025 begins with growth

Back in February, we flagged 2025 as the year that growth would make a comeback and Q1 is tracking in that direction. ARR and GAAP revenue growth are both up quarter over quarter, showing surprising resilience in a choppy market. Top decile ARR growth hit a two-year high, a clear signal that the best companies are starting to break away from the pack.

Startups hit their plans

Plan attainment was 99% this quarter, up from 74% last quarter. And, nearly 50% of companies achieved their Q1 plans as set out at the beginning of the year. This jump may signal a few things. First, that companies have adjusted to the post-free money period, and know how to forecast accordingly. Second, that execution has been solid, even in the face of a turbulent public market. Consistent delivery leads to confidence in the market. This may be a turning point for both.

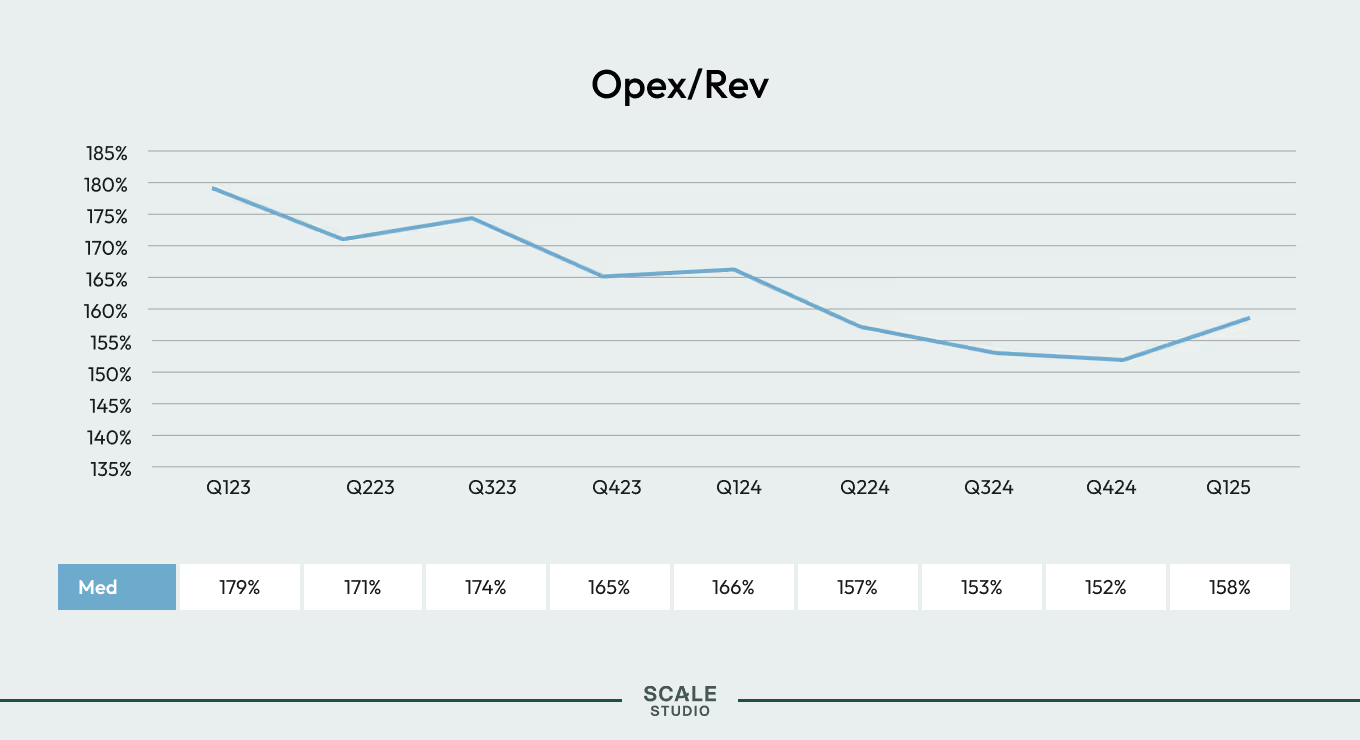

From defense to offense

After steady decreases since 2023, burn multiple and opex/revenue ticked up slightly in Q125. This suggests that startups are beginning to reinvest in growth. It’s possible that after two years there was simply no more to cut and remain a functioning business. But we think it’s more likely that companies are shifting gears and testing out increased spend. As growth comes back, so do operators’ risk appetites.

News from the Scale portfolio and firm