The AI Dividend

There’s been a transformation brewing in how startups operate. Startups are accelerating again, with topline momentum returning in late 2023 and forecasts for 2025 looking increasingly optimistic. What’s striking is that this resurgence in growth is happening while companies are maintaining—and in many cases improving—their operating efficiency. Stabilized opex is a strong signal that the era of “doing more with less” hasn’t ended. Instead, it’s entering a new chapter where AI is quietly powering both sides of the equation: more output by the way of growth, same (or less) input through cautious investment.

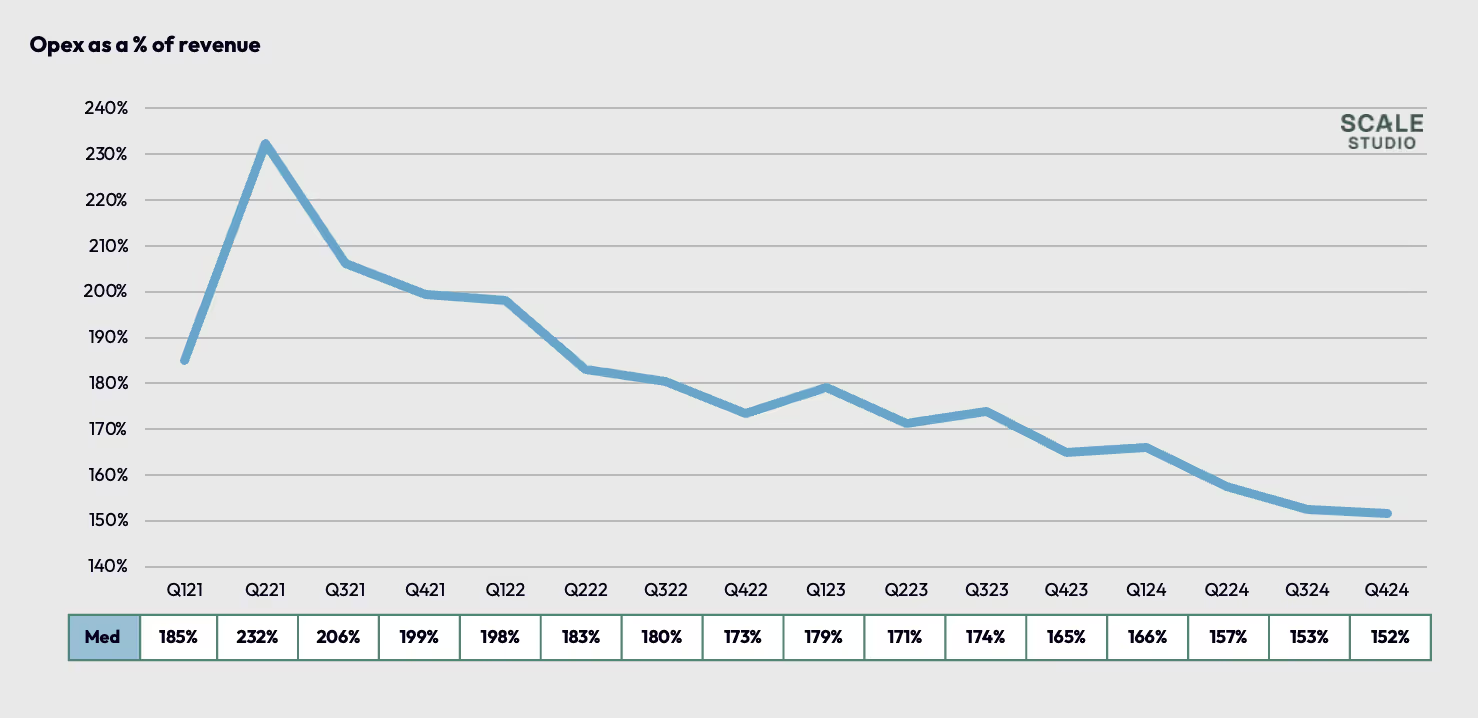

Looking at the latest data from Scale Studio, we’ve seen a consistent and meaningful improvement in operating margin over the past three years. Since peaking in early 2021 at 232% of revenue, median operating expense as a percent of revenue has steadily declined to 152% as of Q4 2024, marking a massive improvement in just three years. Last quarter, we did see an uptick in spend, but it was slight, and what seems to us to be a clear tradeoff for accelerating growth.

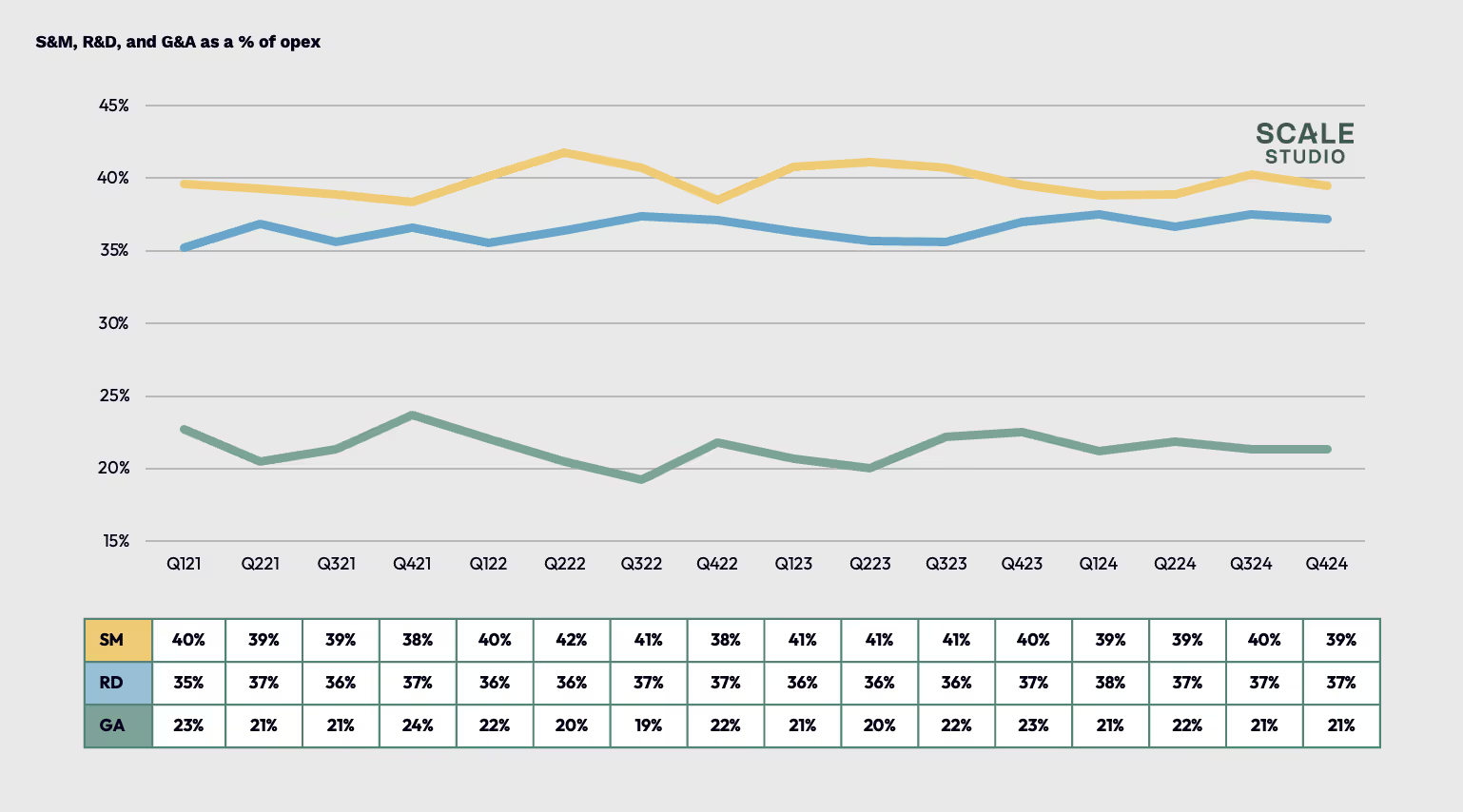

What makes this especially notable: there’s been almost no change in how companies are allocating their operating expenses. S&M, R&D, and G&A as a percentage of total opex have stayed remarkably stable. Sales & Marketing has hovered around 39–41%, Research & Development between 35–37%, and General & Administration around 21–23%.

This means that companies didn’t shift spend between functions to improve margins. They didn’t reduce G&A and double down on product, or vice versa. They simply got more efficient within each line item.

A two-act story

The margin improvement story can be thought of in two parts:

- Act 1: Market driven corrections (2021–2023)

In the wake of the market correction, many startups tightened belts. Despite the AI surge in startup activity, growth was the exception. Teams were reduced, programs were cut, and non-essential spend was paused. These were hard but familiar levers—classic expense control in response to shifting capital dynamics. - Act 2: Slow AI gains (2023–2025)

What’s happened more recently can’t be explained by cost-cutting alone. Growth has returned for many companies. Headcount is stabilizing. That suggests something else is driving the gains.

So, what happened? AI, not just as a technology, but as a pervasive operational layer.

Real deployment, real returns

We’re now seeing strong examples of startups using AI not just to reduce work, but to amplify output.

Take our portfolio company Socure. Their “AI Everywhere” initiative isn’t a cost-cutting measure. They’ve embedded AI into workflows in a way that meaningfully boosts performance without changing the structure of their org, to the tune of a 20% productivity improvement across the board. Tobias Lütke at Shopify is taking a similar stance. In his words, “Before asking for more Headcount and resources, teams must demonstrate why they cannot get what they want done using AI.” That’s a powerful reframe. AI is the new baseline. Human hiring is the exception, not the rule.

In both cases, these leaders are shifting their operating model, with AI as an acceleration factor.

Breaking It down: AI impact by function

With stable opex allocations, it’s worth asking where, specifically, is AI delivering leverage? The answer: everywhere.

1. G&A (Finance, Legal, Ops)

The modern finance stack is becoming AI-native by default. Tools like Klarity, Numeric, and Campfire are integrating AI into finance workflows to automate document processing, explain variances, generate insights, and even draft board decks. The efficiencies are showing up tangibly in G&As bottom line. At our recent CFO Summit, a few standout metrics emerged:

- One multi-billion dollar business is running revenue recognition operations with just four revenue analysts thanks to AI-powered document recognition and order reconciliation.

- Another has saved over 1,200 consulting hours through automated documentation of reporting, data extraction, and audit prep processes.

- Still another has reduced order processing time from 3-4 days to 6 minutes.

2. Sales & Marketing (S&M)

Here, the impact of AI usage is more visible and more measurable.

AI SDRs, powered by platforms like Regie.ai and Qualified, are opening up the top of the funnel in ways that used to require full teams. These tools can generate personalized outreach, sequence messages, and score leads, and even handle calls, often at 5–10x the throughput of a traditional SDR.

The result? Fewer humans needed to hit the same (or better) pipeline goals. Sales reps are often assisted by AI copilots handling prep, follow-up, and objection handling.

Anecdotally, some GTM teams are reporting a doubling of outbound meetings booked and a 17% increase in campaign conversion (stay tuned for hard data on this in the next few weeks).

3. R&D (Product & Engineering)

Productivity gains in engineering are arguably moving fastest, with a huge culture change in their wake.

Developers using AI tools like Cursor, Windsurf, and GitHub Copilot are seeing acceleration the necessary but tedious tasks of debugging, onboarding, and documentation, as well as actual code generation, in extreme cases relegating engineers to approvers instead of coders. Early reports from engineering leaders suggest 55% improvement in productivity, with fewer bugs and better test coverage.

QA is also seeing a lift. Platforms like QA Wolf enable teams to launch with >80% test coverage in weeks, often with only one or two dedicated QA resources. For early-stage companies, that’s game-changing.

Especially in startups where there is no such thing as building products and features fast enough, AI is a huge unlock for builders, greatly reducing time for prototyping, iterating, and getting the boring basics necessary for selling to enterprise done. Shipping faster means growing faster.

What this means for startups

The implications are significant. For now, we’re seeing the changes AI is making in the old world. Within the next few quarters (and definitely the next few years), AI will not be replacing tasks one-to-one. It will be built into the operating model before founders have registered a domain.

This resets how we think about growth. $300K ARR per FTE used to be great. Now, companies are targeting $1M+ with AI-augmented teams. Every new hire will have to be defensible.

The takeaway

AI is now showing up where it matters most: the income statement.

The evidence in the Scale Studio charts is subtle but telling. Margins are improving not because companies are cutting more, but because they’re doing more with the same. And for the first time in a while, we’re seeing durable efficiency gains without major reallocations or reinvention.

This is the AI dividend—quiet, compounding, and increasingly embedded in how startups operate.

The teams that figure out how to harness it early won’t just survive the next wave of change. They’ll define it.

News from the Scale portfolio and firm