The Re-Acceleration Is Real

Late last year when all our companies were planning for 2021, many teams put out aggressive plans for re-acceleration in 2021. I remember pushing back and worrying that these plans were too lofty. Now the first Q1 numbers are in and boy was I wrong.

The chart below shows the growth rate of Total ARR and the growth rate of Net New ARR, across the portfolio for the last nine quarters. When Net New ARR is growing faster than Total ARR, that is the early signal that ARR growth rates are about to accelerate (it really is just math). Twenty years of data shows us that, in any given quarter, fewer than 30% of companies are accelerating and most de-accelerate at a fairly steady rate, fortunately from a high initial starting point.

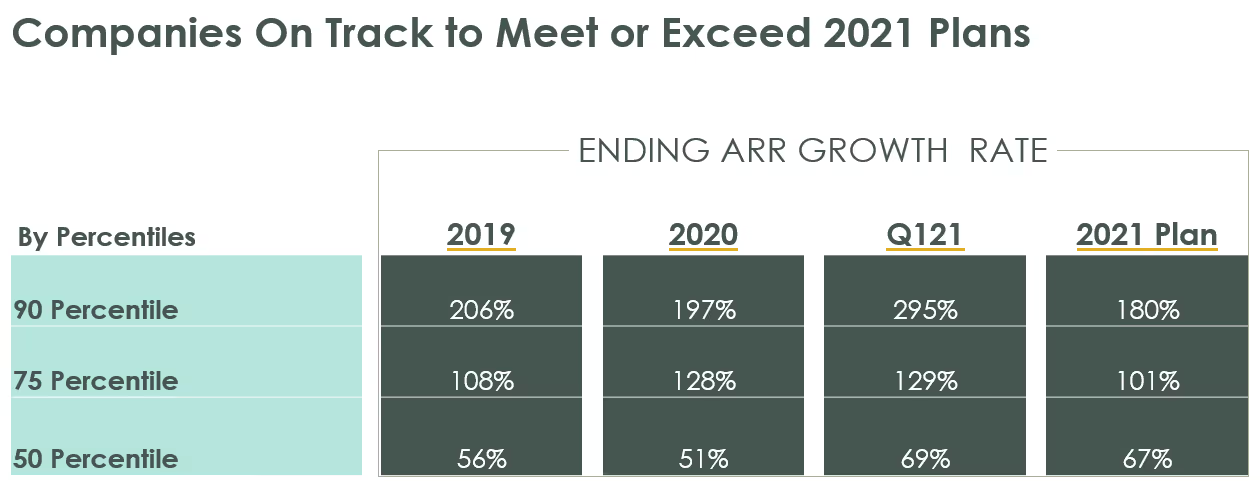

Not so in Q1. For the second quarter in a row, the median Net New ARR growth rate across the portfolio was greater than the ARR growth rate, this time substantially so. This means companies are coming out of the COVID funk, investing in distribution, and seeing success.

This is a clear bullish sign on company performance and an incentive to lean in on investing in GTM for the next few quarters. The COVID shutdown validated the cloud, and a sizable chunk of the post-shutdown cash that is now starting to flow through the economy is coming the way of cloud software companies.

Based on these early returns, the full-year plans for the companies we work with no longer seem so fantastical. The data is early and noisy (especially at the 90th-percentile level) but a median re-acceleration from 51% to 67% clearly looks doable.

Two caveats, and one shout out.

The caveats: First, this is early data from about half the companies in our portfolio. Despite the Godfather warning, bad news tends to come slower so there could be some downward adjustment here. Second, and more importantly, this is absolutely not a bullish comment on company valuations. It is a “No comment.” Just like the public markets, how companies are valued is not a function of performance but rather how well that performance compares to expectations. Expectations are currently running high, based on the valuations we are seeing.

Finally, the shout out. This data comes from the work done by Dale Chang, our Partner running Portfolio Ops, and his team, together with all the portfolio companies who report quickly. Dale will share a more detailed quarterly Flash Report when all the Q1 data is in.

News from the Scale portfolio and firm