Virtual Reality: Ready for Prime Time? Or Gamers Only?

.png)

It is still early in the VR adoption cycle; 2016 was an introductory year, with first-gen products launched by Oculus and Vive, consumer familiarity rising, even a WSJ column from sports columnist Jason Gay. This year, 2017, will be the year we determine if VR adoption goes the way of the iPhone or the Windows Phone.

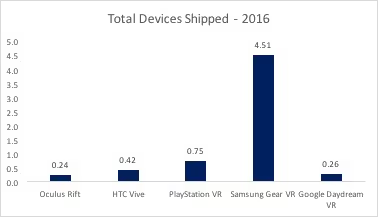

Virtual reality has had its share of failed promises as documented by the media, but this could be a result of misguided expectations rather than muted numbers. Five major technology companies have established a foothold in the sector – Alphabet, Facebook, HTC, Samsung and Sony – with commercial traction to back it up. Samsung shipped 4.5M Gear mobile headsets and (Facebook) Oculus Rift + HTC Vive combined to total 650K units. For comparison, Apple sold just 1.4M units of the iPhone in the first year (2007).

These numbers require some narrative, as Sony Playstation was supply-constrained after opting to manufacture a smaller batch in the first run, and Google Cardboard is excluded entirely, as the majority were distributed for free rather than purchased.

Is 2017 the year VR gets to 10M+ units and broader adoption or does it remain a gaming-only phenomenon that appeals to only the hardcore? Having followed the space for the last year, a few trends stood out to me that could make 2017 the year for greater adoption. Should these prove out, VR may work its way out of the underwhelming category come year-end.

- ‘Magic window’ will continue to serve as a way for consumers to organically come across 360 degree content within their web browser or mobile app. This format requires no extra download, no head-mounted display, and the touch engagement will come naturally for people on mobile phones. Magic window content will become commonplace for web and mobile properties geared toward travel, entertainment, real estate, or other industries with heavy spatial elements. Google has VR view, Mozilla has A-frame, and other dev frameworks exist. As consumers encounter more 3D content, they will come to expect it.

- We are moving (have moved?) to a world where everyone is a visual content creator. Magic windows and partnerships like that of SketchFab + Facebook to embed 3D files have made distribution possible. Consumers are already active 2D content creators (see Snap and Facebook for details) and 3D capture should follow. Free or inexpensive options already exist for real world capture and computer generated capture.

- As consumers know firsthand, the hardware is first-generation, and with that comes adjectives like expensive, clunky, uncomfortable, and tethered. Expensive HMDs must get cheaper and less cumbersome. Mobile phone versions must process faster and render more clearly. The extremes of HTC Vive / Oculus Rift and Google Cardboard / Samsung Gear will evolve to look more like one another. QuarkVR + HTC Vive have a prototype for a less* tethered, Wi-Fi streamed product. Imagine no longer tripping over cords as you turn to shoot or paint.

- For mainstream adoption we need to see examples of startup companies and new entrants making inroads (and revenue) in VR. When developers start making money in VR, the flywheel will be in motion. The vocal early traction is from Alphabet, Samsung, HTC, Facebook, and Sony, but what these companies have in common is they can self-fund losses in VR with profits from other lines of business. We have examples of flame outs already; we do not have obvious examples of VR-driven success.

- One non-trend that should give us all pause is Apple. Per SuperData and Unity, in the United States developers make 45% more on an iOS gamer than an Android gamer. With consumer VR mostly a gamer’s world today, the absence of Apple is noticeable. Will it weigh down the industry if Apple does not deliver a headset like Cardboard, Daydream or Gear? The best mobile VR experiences today are vertically integrated, with Google Pixel + Daydream, and Samsung Gear VR + Galaxy. What does it mean if Apple goes straight to augmented reality?

The road is long but these observations suggest that 2017 could be a year of increased consumer VR adoption and evolution on the supplier side. As a VR household, I am anxious to participate. As a keen investor, I am tracking closely. As an enterprise investor, the adoption curve looks different but I believe a handful of applications exist with killer functionality. I’ll cover enterprise VR and AR in future blogs.

Disclaimer: I own an HTC Vive and am a converted non-gamer. I’m comfortable admitting that my favorite games include: Tiltbrush, AudioShield, RawData, RecRoom, and Valve’s Lab. I’m told I should try Island 360 and Soundboxing. I welcome other suggestions.

* I say ‘less’ tethered because the tether will connect to a transmitter gizmo in my pocket to stream between the headset and the PC. The transmitter is connected to the cords but at least it’s on my body!

News from the Scale portfolio and firm