Growth Slows while Companies Sprint to Efficiency: Scale Studio Flash Update

Our quarterly Scale Studio Flash Updates analyze a representative sample of enterprise software startups to measure industry growth rates and the health of the SaaS market. The most recent updates were 2023 Whisper Numbers, Q322, Q222, and Q122.

What You Need to Know Right Now

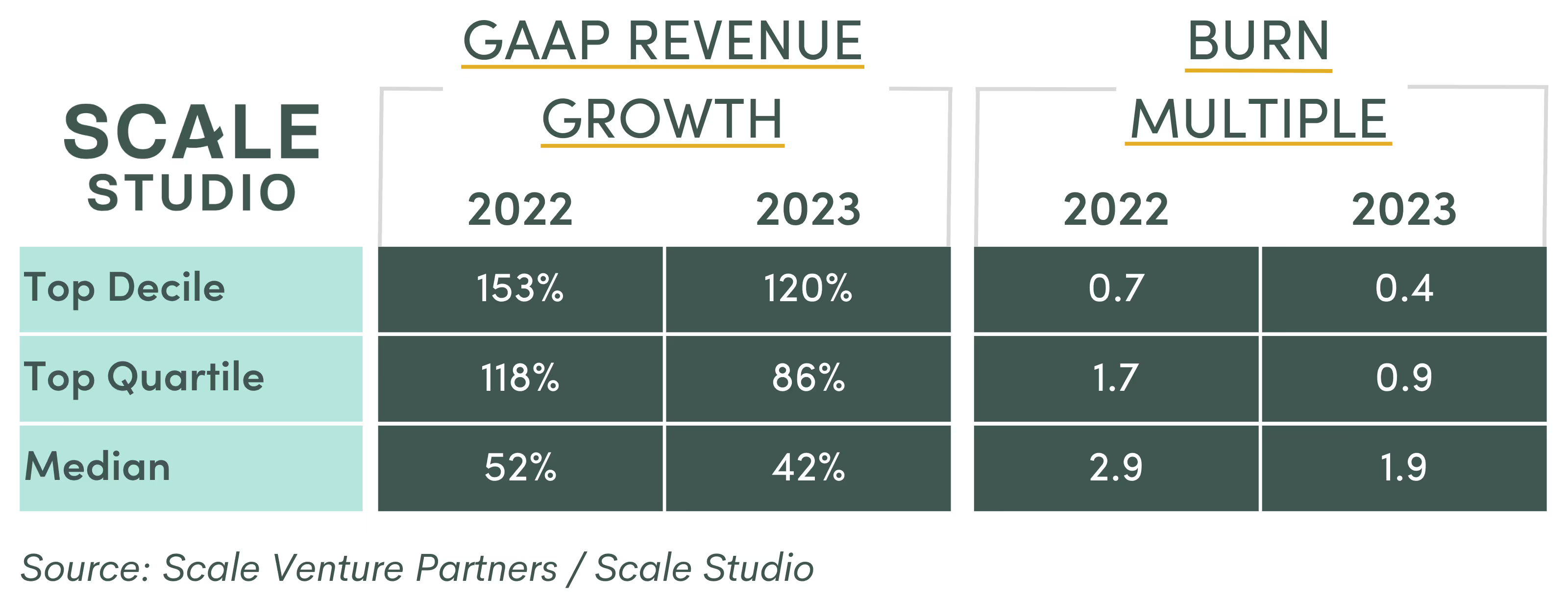

No one can tell exactly what 2023 will bring, but one thing is for certain: there is a sprint to efficiency with improving burn multiples and slowing revenue growth across the board. Comparing 2022 performance with 2023 plans shows the stark reality. The slowdown in ARR Growth we saw in 2022 will result in a slowdown in GAAP Revenue Growth in 2023. At the same time, startups have tightened their belts to become more efficient. For example, the top quartile revenue growth rate is forecast to drop by 25% relative to 2022 levels, while at the same time the top quartile efficiency is forecasting an improvement of 50% relative to 2022. The chart below shows 2022 performance and 2023 plans for those companies that have reported across our portfolio.

Only time will tell what will end up happening this year (remember how different the world was in early-February 2022?), but we can perhaps get a sense of how companies are adjusting to the new market environment by looking backwards at the last quarter of 2022.

Some Context: Q422 Performance Highlights

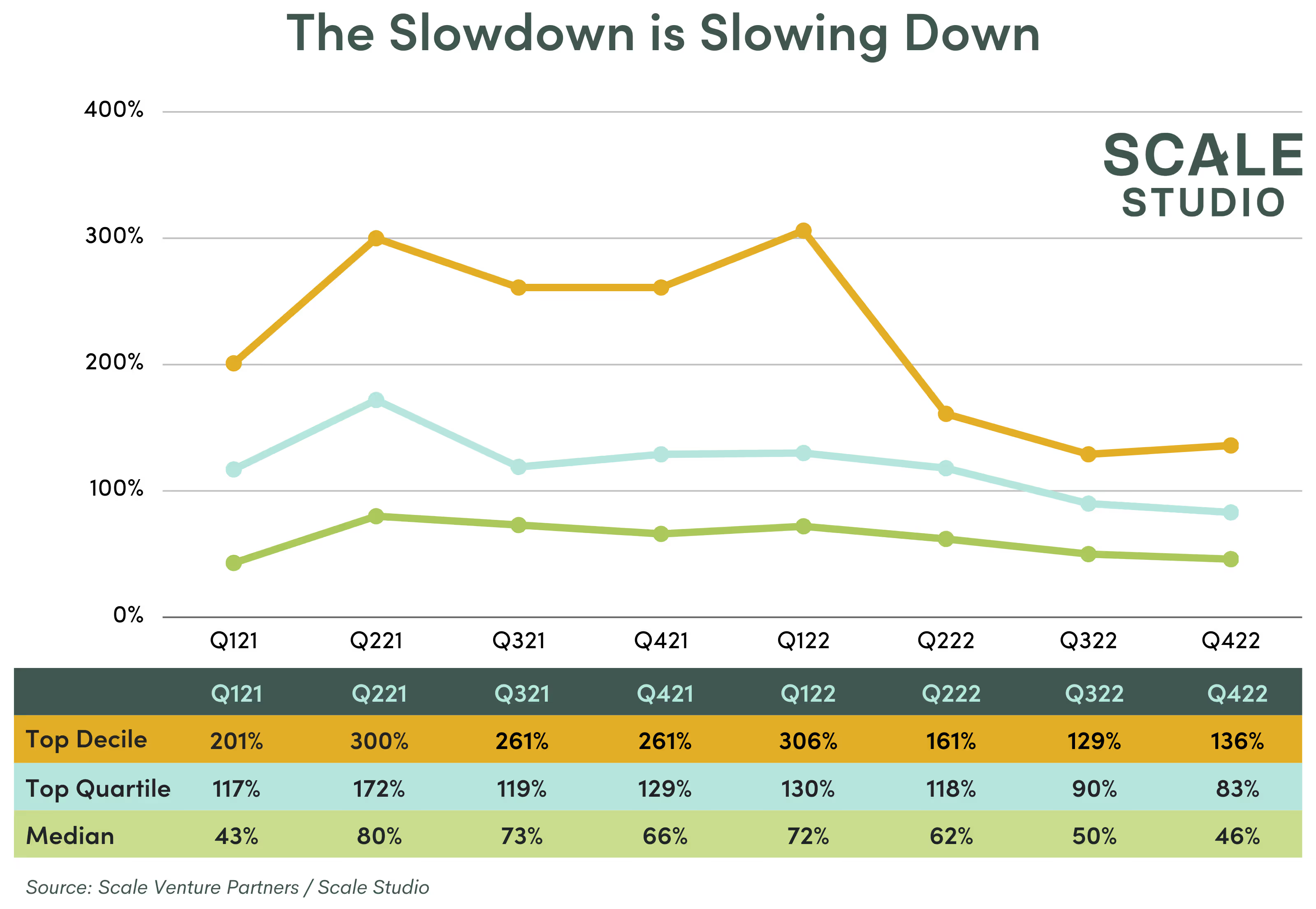

- 46% Median ARR Growth Rate was lower than Q322 results of 50%

- 136% Top Decile ARR Growth Rate was slightly higher than Q322 results of 129%

Q422 Growth Rate Analysis

Q422 was a continuation of the slowdown in growth we saw throughout 2022, with growth rates returning to their pre-pandemic levels. Top-decile growth has remained steady at 136%, slightly higher than the 129% in Q322, but still much lower than the 300%+ growth rates we saw in 2021 and early 2022.

Top quartile and median companies continued to see declines in growth rates, with top-quartile growth falling from 90% to 83% and median growth falling from 50% to 46%. On a more optimistic note, the slowdown is itself slowing down, with top-quartile growth only falling 7% in Q4 versus 28% in Q3 and the median growth falling 4% in Q4 versus 12% in Q3.

2023 Forecasts Indicate a “Sprint to Efficiency”

Now that we’re already halfway into Q1, most companies have either finalized their 2023 plans or are very close to a final plan. We took a look at these 2023 plans and compared them to the now-final 2022 numbers from our companies to see where we’re headed in 2023. Two things stand out when comparing 2022 and 2023 (and have been the focus of many a board conversation): growth and burn.

Due to the slowdown in adding new ARR in 2022, companies are forecasting a continued decline in GAAP Revenue Growth rates this year. The lower GAAP Revenue growth puts an increased focus on runway and cash burn, as companies think through how they’ll survive until growth picks up again.

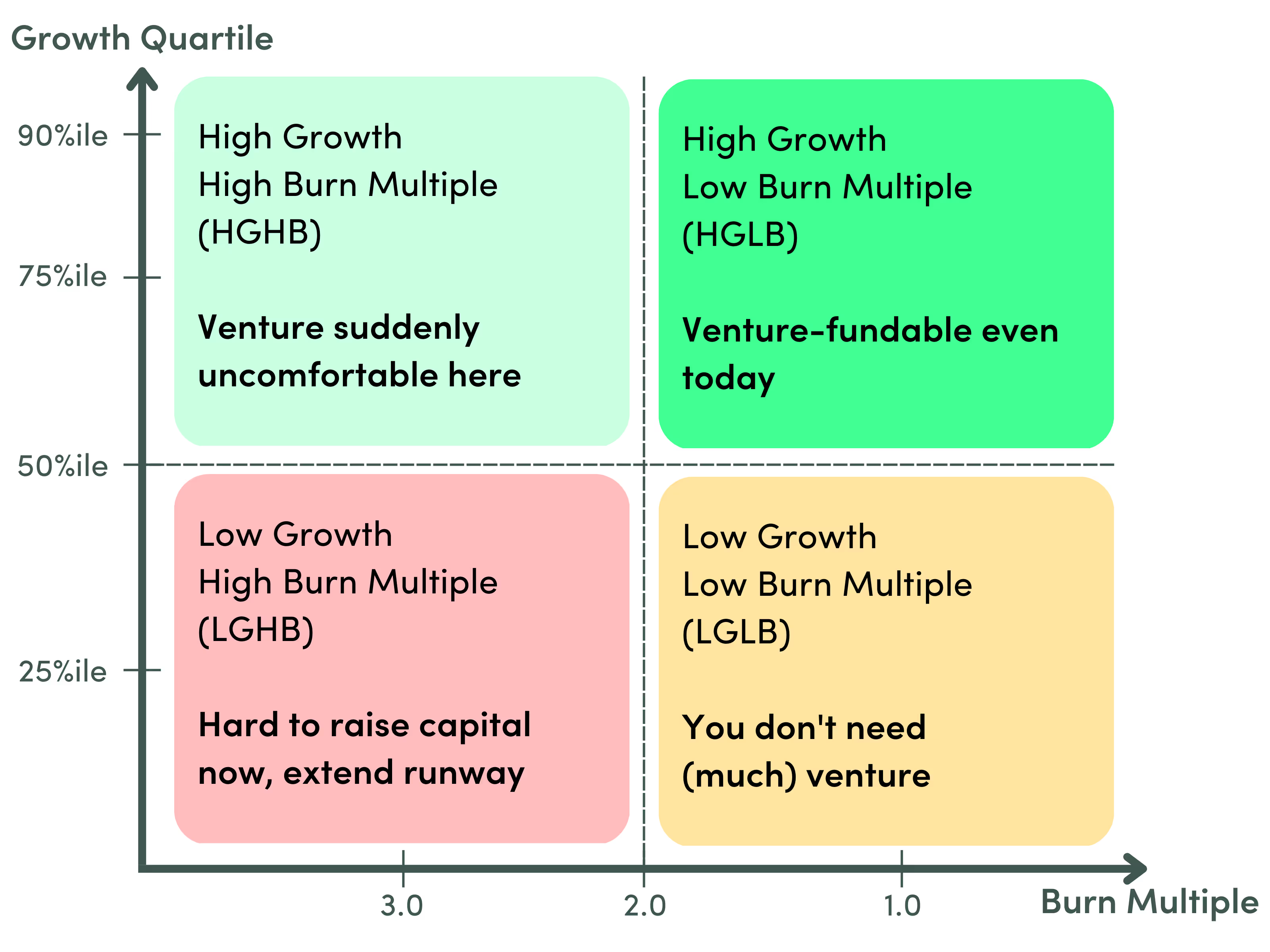

We’ve seen layoffs across the board in the tech sector, as both startups and industry giants had to right-size their organizations for the new growth landscape. Looking at the chart above, one of the starkest differences between 2022 and 2023 is the change in burn multiples. Across our portfolio, every company is sprinting towards efficiency in 2023, with some looking to reduce their burn multiple by 30-50% or more. Together with lower growth, this means companies are pushing towards the lower-right quadrant in our Growth vs Burn Matrix:

Companies are Cautiously Optimistic for 2023

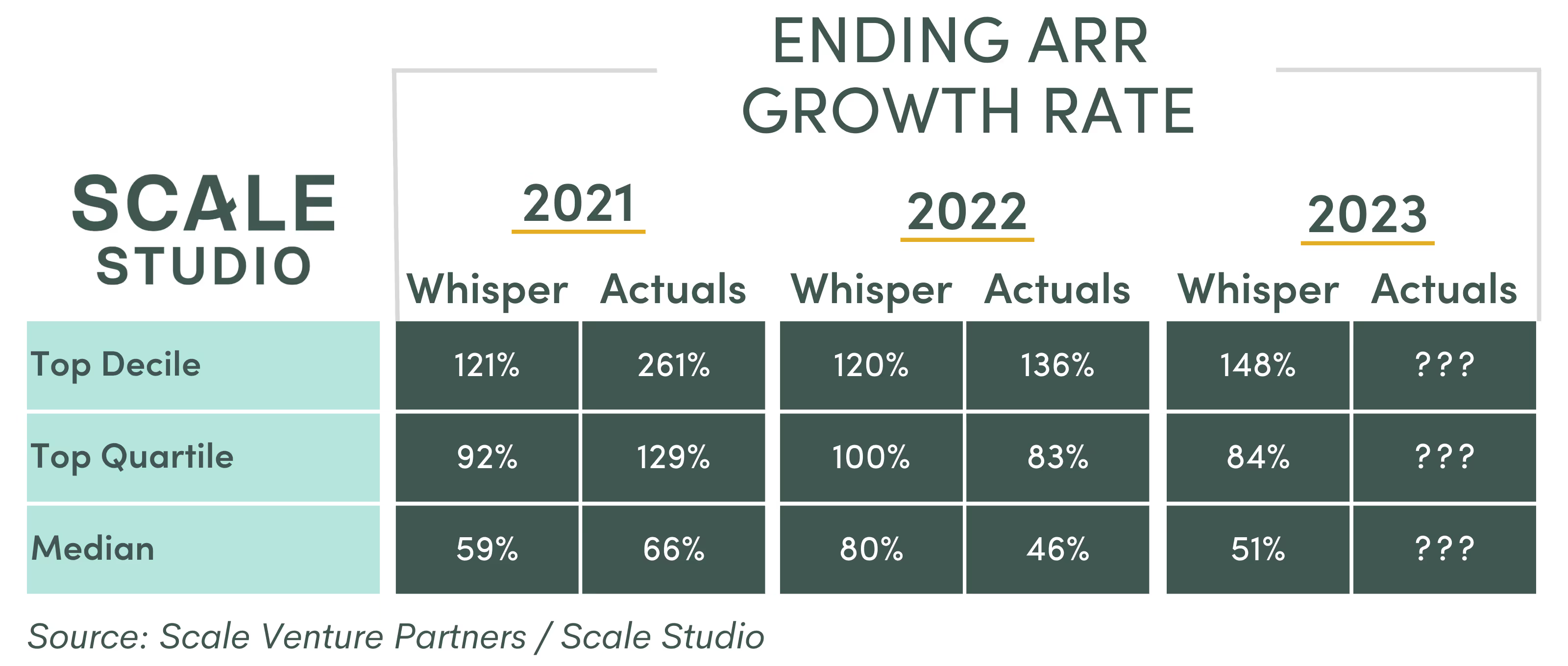

When comparing the ending 2022 ARR growth rates and forecast 2023 ARR growth rates, we see that companies are forecasting that the decline in ARR Growth will level off this year, potentially inching upwards slightly. However, looking back at initial forecasts for 2021 and 2022, companies have a mixed record of achieving the plans they set forth at the beginning of the year. As shown in the chart below, in 2021 we saw companies over perform their initial forecasts (particularly the top quartile / decile companies) but in 2022 most companies underperformed their forecasts due to the dramatic shift in the markets throughout the year.

We’ll have to see where companies end up at the end of 2023, but given how we saw companies adjust their forecasts throughout 2022, we’re hopeful that companies have adjusted their forecasts for the new macro environment and will end the year closer to their original plans than in past years.

Recent Flash Reports

News from the Scale portfolio and firm