Scale Studio Flash Update: Economic Gravity Pulls on Software Startups

Scale Studio Flash Updates analyze a representative sample of enterprise software startups to measure industry growth rates and the health of the SaaS market. The most recent updates were Q222, Q122, 2022 Whisper Numbers, Q421, Q321, and Q221. Find out about Scale Studio here.

What You Need to Know Right Now

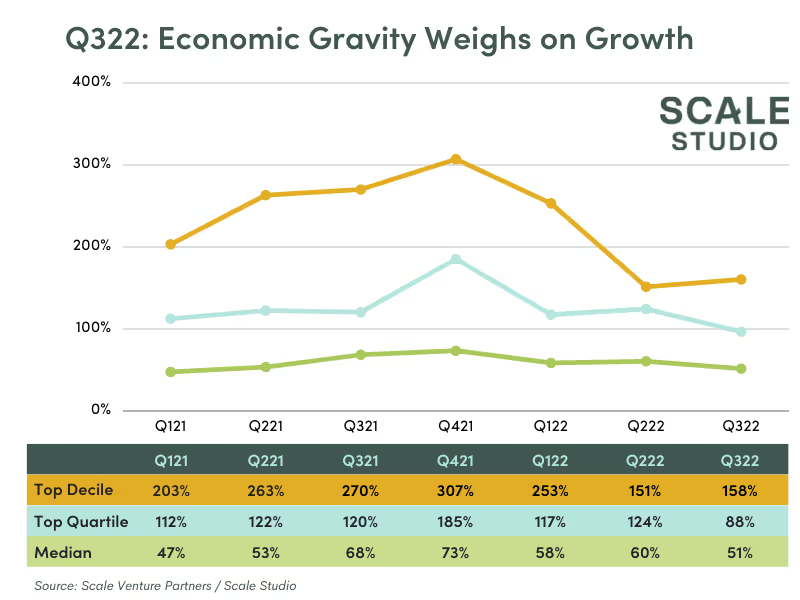

- Median ARR growth rate fell to 51% in Q3 (compared to 67% last quarter) as economic headwinds hit software spend.

- Top quartile growth slowed down this quarter to 96% (compared to 134% last quarter) while top decile growth has stabilized (for now) matching last quarter’s 160% (far below prior highs).

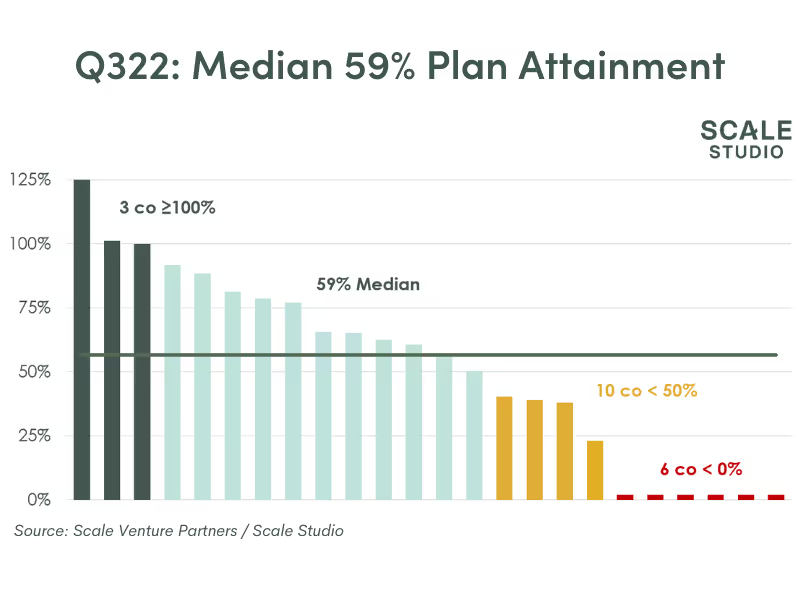

- Only 13% of companies are achieving plan (compared to 28% last quarter) with a corresponding drop in median plan attainment of 57% (compared to 73% last quarter).

Performance Highlights of Q222

- 51% Median ARR Growth Rates lower than prior quarter final results of 67% in Q222 and 58% in Q122.

- 160% Top Decile ARR Growth Rates identical to previous quarter. Though this is a dramatic drop in growth compared to 253% in Q122.

- 13% of companies overachieved against Q322 plans. This is lower than even the original Covid Shock in Q220.

- 57% Median Plan Attainment down from our Q222 final result of 73%. Plan Attainment compares a company’s actual ARR for a period to its annual plan ARR target for that period.

Growth Rate Analysis

Economic gravity has started to hit all parts of the software landscape with drops in performance across all quartiles in the past several quarters. As mentioned in our Q222 update, our biggest concern was the buckling of growth rate for top decile companies, dropping from a high of 307% in Q421 to a low of 160% in Q222. That number has stayed steady this quarter, with early returns showing 160% ARR growth for the top 10% of companies which is identical to the prior quarter.

But, what is concerning is that the resilience of the next tier of companies is being tested. Early returns show a 96% growth rate which represents a dramatic drop compared to 134% from Q222. We’re even seeing a drop in performance for the median company which turned in 51% median growth rate compared to 67% in the prior quarter.

While it’s hard to determine how much of the drop in growth is attributable to software companies pulling back on aggressive sales and marketing spend vs. customers pulling back spend as they rationalize their software subscriptions, anecdotally it seems as though we are shifting from the former to the latter.

Plan Attainment Analysis

Not surprisingly, attainment of plan has also dropped in Q322 — with only 13% of companies achieving or exceeding Q3 plans. We also noticed a corresponding drop in median attainment to 59% of plan. This result compares unfavorably with when we reported in Q2 of this year with median plan attainment of 73% of plan. Even more concerning, this is even lower than what we saw in Q220 during the initial Covid Shock.

Planning for 2023

With the bulk of 2022 behind us, attention now turns to planning for 2023. The topic of conversation in every boardroom is the corresponding tradeoffs between growth and burn. Check out the tool that we built that helps you understand how you compare with other companies. Stay tuned as we’ll also be publishing our 2023 Whisper Numbers later this month.

Recent Flash Reports

News from the Scale portfolio and firm