Growth slows beyond expectations in Q1: Scale Studio Flash Update

Scale’s quarterly Scale Studio Flash Updates use our proprietary data platform, Scale Studio, to analyze a representative sample of enterprise software startups and provide a nearly real-time look into industry growth rates and the health of the SaaS market. Today, we explore the results of Q1, 2023.

What you need to know right now

At the beginning of the year we saw that companies were cautiously optimistic with their 2023 plans, forecasting a small increase in growth compared to 2022. There was some hope that the worst was behind us economically, and that plan adjustments, along with improvements in efficiency, would be suitable for the new macro environment.

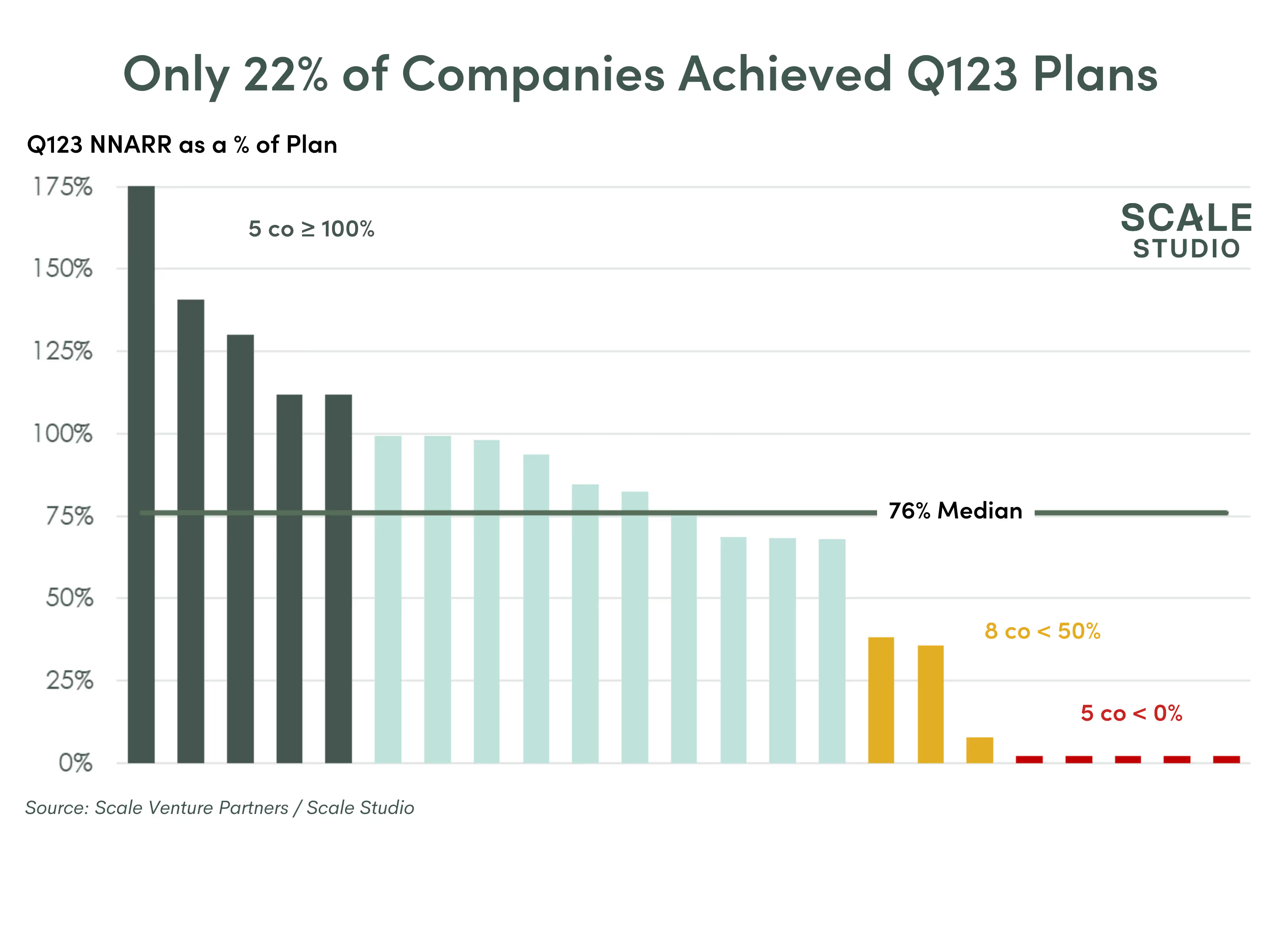

Q123 data indicates that the growth slowdown is continuing – and most companies failed to meet even the conservative plans they set earlier this year. This was the fourth consecutive quarter of decrease in both top-decile and median year-over-year ARR growth, with only 22% of companies achieving their Q123 plans.

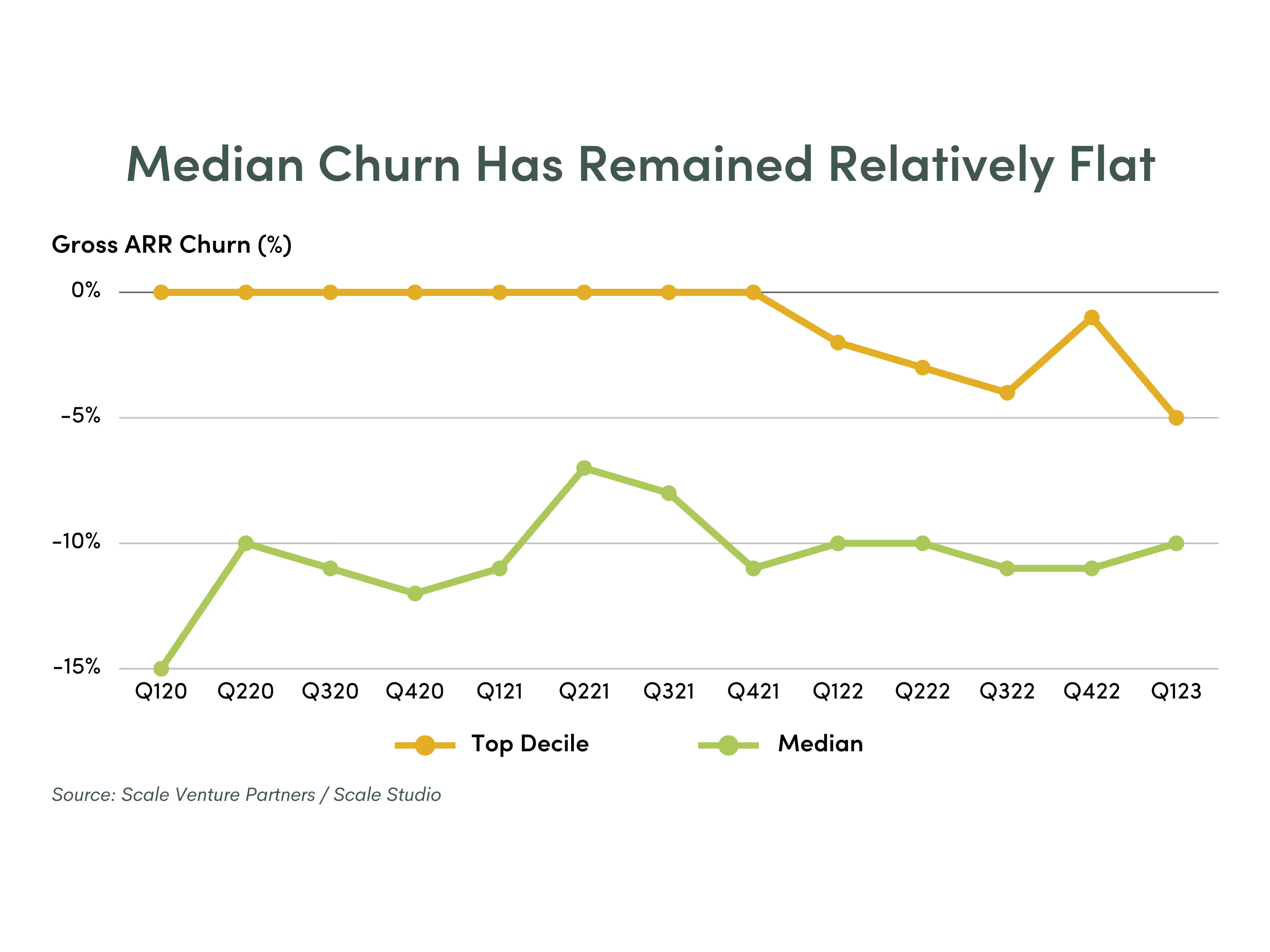

Surprisingly, we did not see a sharp increase in churn in Q123 – which we hypothesized we might see given the cost-cutting measures across the industry. Instead, we saw companies optimize their spend by pushing back more on upsell and pricing, and a general slowdown in new deals in Q123. Was this slowdown mostly driven by the SVB crisis? Or is this a sign for how the rest of the year will play out?

Q123 performance key findings:

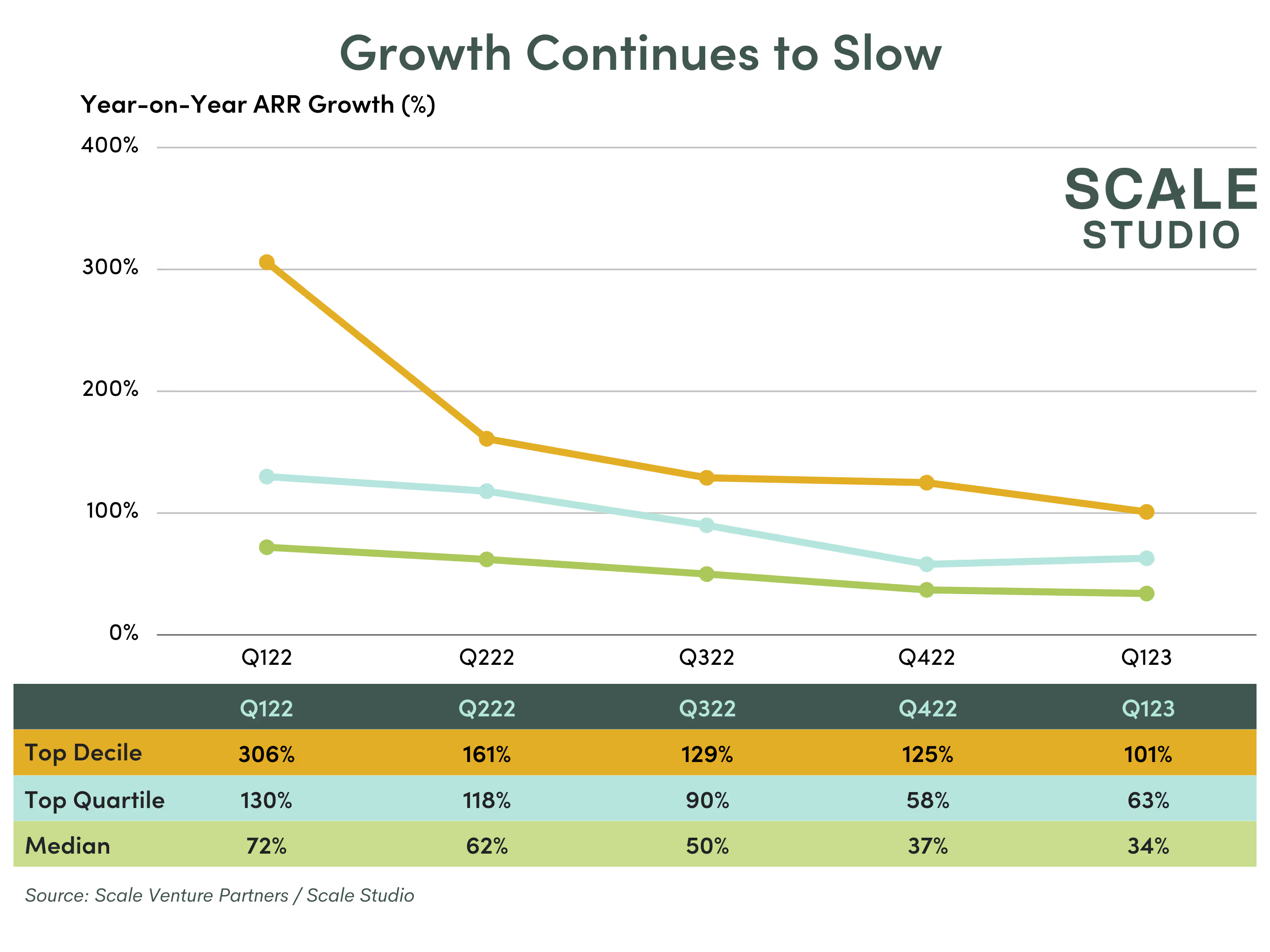

- Median ARR Growth Rate was 34%, lower than Q422 growth of 37%

- Median Plan Attainment was 76% , the same as Q422

- 22% of Companies Achieved Q122 Plans, versus 34% in Q422

Q123 growth rate analysis

Growth rates are continuing to tick downwards, with median ARR growth of 34% now falling below pre-Covid levels. Looking at the top performers only, even the top-decile growth rate of 101% has continued to fall – showing that even the fastest-growing companies aren’t immune to the continued slowdown. As you can see below, Q123 is the fourth quarter in a row that both the top-decile and median growth rates have fallen. Compared to historical growth rates, the 34% median ARR growth we saw in Q123 is less than half of the 72% growth we saw in Q122, and is even lower than the ~40% growth we saw in 2020 at the beginning of the pandemic.

Q123 plan attainment analysis

Somewhat surprisingly, only 22% of companies met or exceeded their plan for Q123. This is especially surprising since under normal circumstances, Q1 should have the highest percent of companies meeting plan. Companies finalized these plans just a few months ago, meaning the deviation from plan is occurring rapidly and unexpectedly. For reference, plan attainment was 38% in Q122 and 59% in Q121. Even in Q122, with inflation taking off and the economic uncertainty brought forth by Russia’s invasion of Ukraine, more companies achieved their plans than in Q123.

Looking at the median plan attainment (or what percent of their plan companies actually managed to reach), in Q123 it was 76%. This is much lower than 93% in Q122 and 100% in Q121, but the same as the 76% plan attainment we saw in Q422.

So why are companies falling short on their growth targets? And is this a temporary blip from an exceptionally strange quarter for the startup ecosystem, or indicative of a harsher than expected 2023 with more yet pain to come? We dug into the data to see what it says.

Is churn to blame?

Initially, we thought we’d see a spike in churn in Q123 as customers adopted cost-cutting measures including reducing SaaS spend. But the chart below shows the median and top-decile gross churn for the last 3 years, which has remained roughly the same since the post-Covid recovery, with just a slight increase in top-decile churn in the last year. Given the relative consistency of median churn rates, it is unlikely that the plan misses were heavily driven by an increase in churn.

What about new ARR?

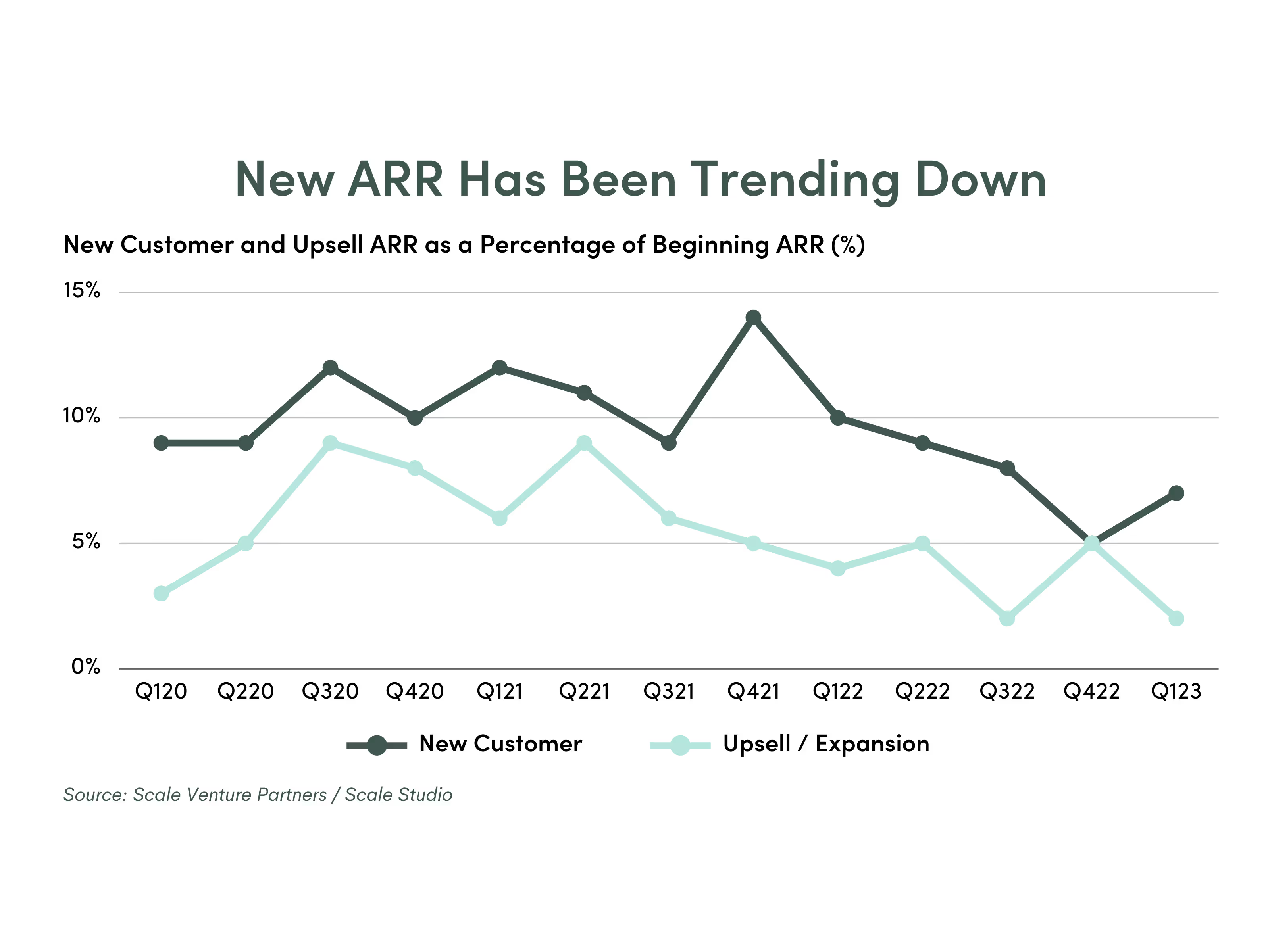

Since it seems that companies aren’t churning more ARR than expected, perhaps the culprit behind the plan misses is a reduction in the additional ARR companies are bringing in from new customers or upselling their existing customers. Looking at the change in median new customer ARR and upsell ARR as a percentage of beginning ARR in the chart below, we can see that both new customer and upsell ARR have been decreasing over the past couple of quarters. During the peak of the post-Covid recovery, the median company was adding up to 14% in new ARR from new customers and 9% from existing customers. Now, those numbers have fallen to around 7% and 2%, respectively.

Looking at the data above, it seems likely that new IT spend was among the first cuts companies made, but that didn’t necessarily mean canceling existing SaaS services. Anecdotally, we’ve heard from some companies that the reason they’ve missed new ARR targets is dragging sales cycles, and a number of deals have slipped into Q2, which likely indicates CFOs are becoming more thorough in their examination of new software purchases than sellers are used to. Hopefully, some of those deals will close in the near future and help companies get back on track towards hitting their annual 2023 goals.

A more pessimistic possibility is that as we get farther into the year, companies take even more drastic cost-cutting measures and start canceling (or not renewing) their existing SaaS services, driving up the churn numbers we looked at before.

Which will it be? We’re paying close attention. We’ll make sure to check in with both churn and new ARR in our Q223 Flash Update to see which case ends up playing out.

Recent Flash Reports

News from the Scale portfolio and firm